Chipotle Stock Wins a JPMorgan Upgrade After Falling 43%: Here’s Where It Could Go by Year-End

Key Stats for CMG Stock

- Past week’s performance: 9.7%

- 52-week range: $28 to $58

- Valuation model target price: $47

- Implied upside: +46.5% over 2.5 years

Value CMG alongside its fast-casual peers with TIKR (It’s free) >>>

JPMorgan Flips to Overweight, and the Market Starts Listening

Chipotle Mexican Grill (CMG) climbed roughly 6% on June 5 after JPMorgan upgraded the stock from Neutral to Overweight and set a $35 price target. That move helped push the stock’s two-week gain to roughly 5.7% from a trough near $28, its lowest close since 2021.

Chipotle shares had fallen 43% since May 2025 while the S&P 500 gained 29%. At or below $30, the firm said the stock presents more risk-weighted upside than downside. The analysts noted that management, in the meeting, clearly acknowledged past operational missteps, particularly the portion-size inconsistency that drove a wave of customer complaints through 2024 and into 2025.

CEO Scott Boatwright said in Chipotle’s Q1 release: “Our first quarter exceeded expectations as we advanced our Recipe for Growth strategy, delivering tangible progress across operations, digital, menu innovation, people, and development.”

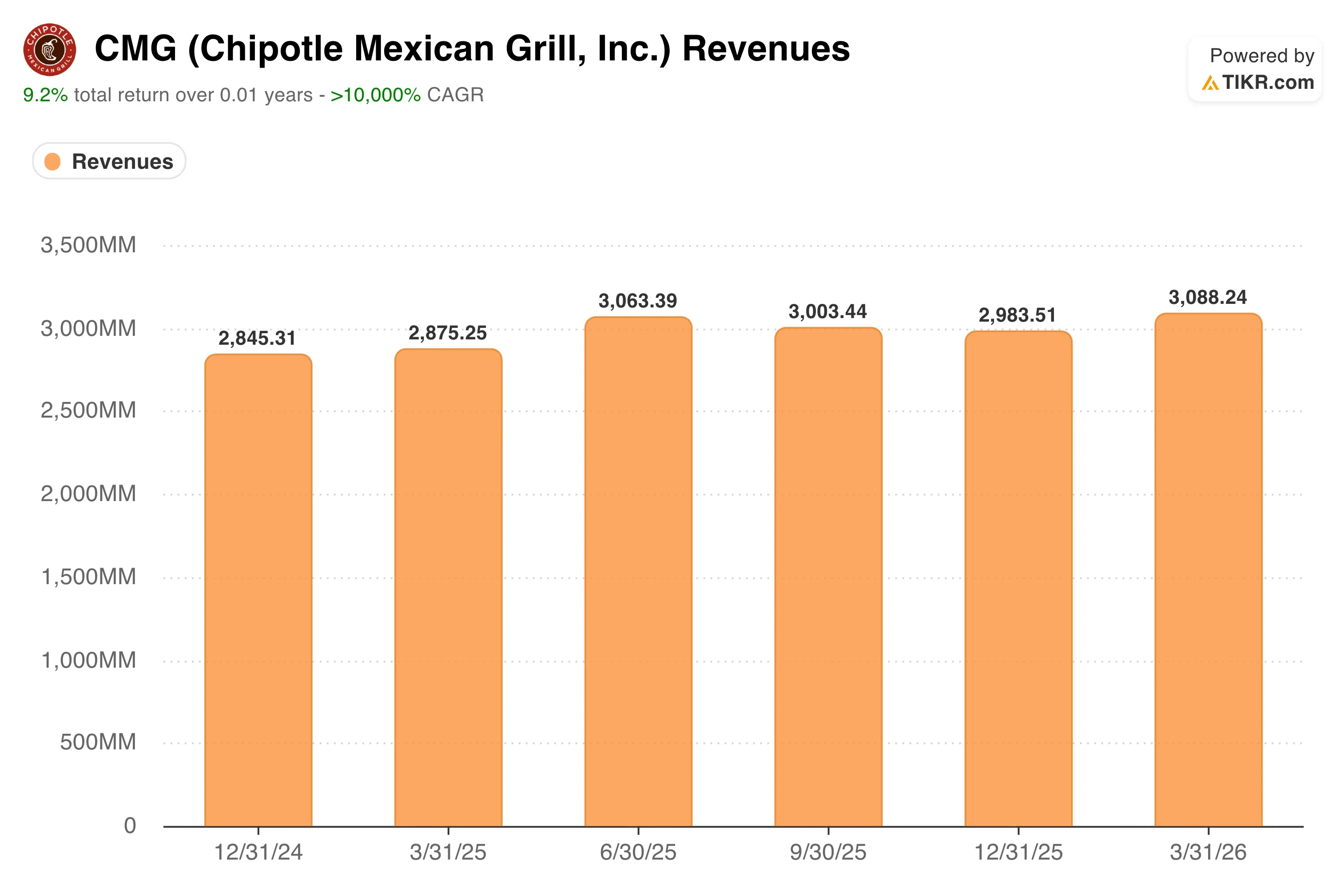

CMG Revenues (TIKR)

CMG Revenues (TIKR)

Q1 2026 results, reported April 29, reinforced the cautious optimism. Revenue reached $3.09 billion, slightly ahead of the consensus estimate of $3.07 billion, driven by new restaurant openings and a return to positive comparable sales of 0.5%, which was far better than the 0.7% decline Wall Street had expected.

GAAP diluted EPS was $0.23, down 17.9% from the prior year, reflecting higher labor costs and rising beef prices. Adjusted diluted EPS came in at $0.24. CFO Adam Rymer called the guidance “conservative,” citing unpredictable consumer trends linked partly to fuel price volatility from the U.S.-Iran conflict.

Going forward, CMG stock’s path will depend almost entirely on whether Q2 comparable sales, due July 29, show a genuine recovery or another quarter of flat-to-muted traffic.

See analysts’ growth forecasts and price targets for CMG (It’s free) >>>

Is Chipotle Stock Undervalued at Current Levels?

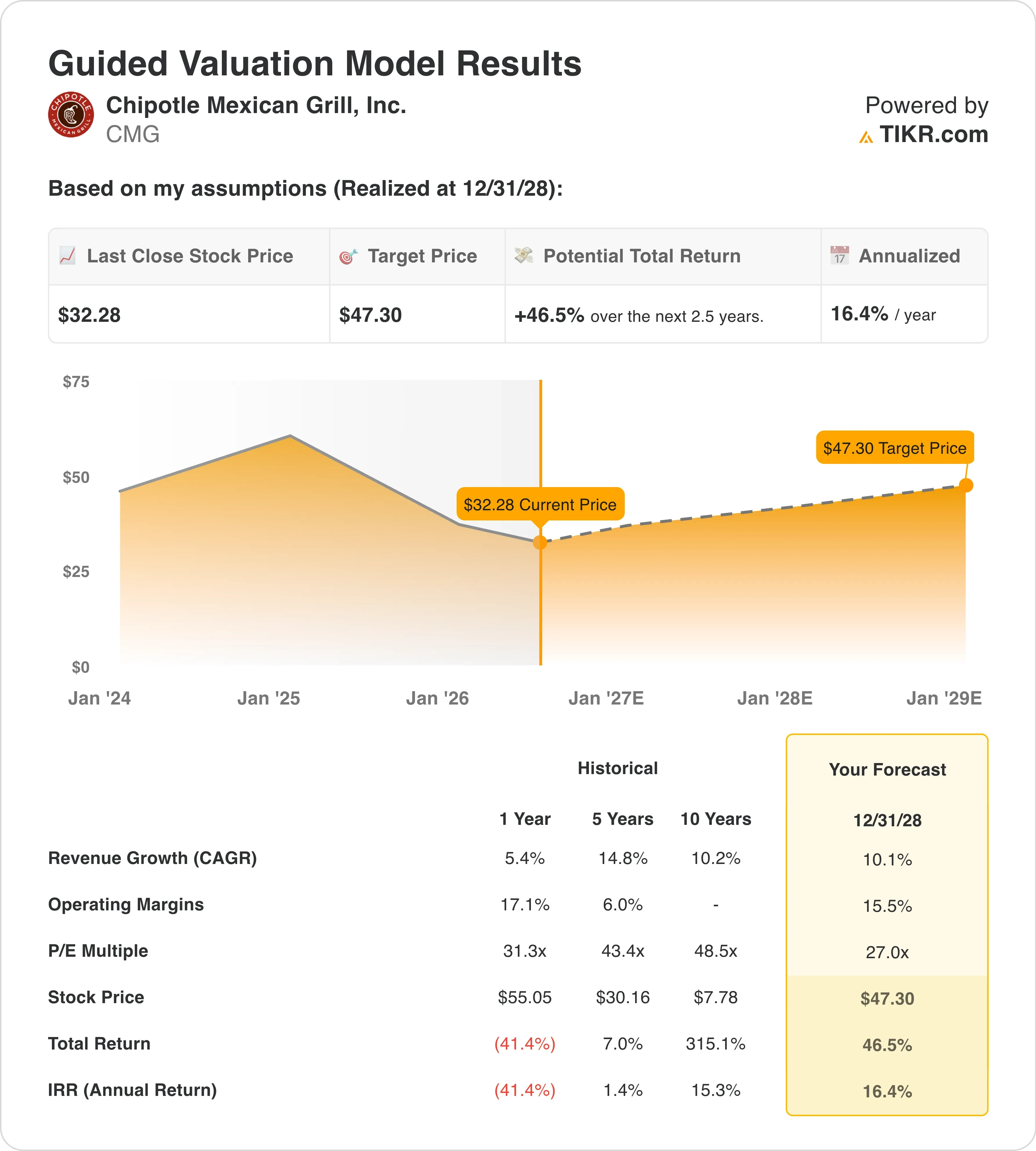

CMG Guided Valuation Model (TIKR)

CMG Guided Valuation Model (TIKR)

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue Growth (CAGR): 10.1%

- Operating Margins: 15.5%

- Exit P/E Multiple: 27.0x

Based on these inputs, the model estimates a target price of $47, implying 46.5% total upside from the current share price of $32 and a 16.4% annualized return over the next 2.5 years.

A 16.4% annualized return is genuinely attractive for a large-cap restaurant company. The 10.1% revenue CAGR assumption is conservative relative to Chipotle’s 10-year historical revenue CAGR of 10.2%, meaning the model essentially asks the company to repeat its long-term average. That is not a heroic assumption. It is anchored in 350 to 370 new restaurant openings per year and modest average unit volume recovery as comparable sales stabilize.

The 15.5% operating margin assumption sits slightly below the Q1 reported operating margin of 12.9% but reflects a gradual recovery as labor cost growth moderates and throughput improvements from new kitchen equipment take hold.

CMG Guided Valuation Model (TIKR)

CMG Guided Valuation Model (TIKR)

Chipotle’s longer-run margin structure has proven resilient because its food preparation model avoids fryers and industrial cooking equipment, keeping both capex and kitchen labor lower than many peers. The company expects technology investments, including high-efficiency kitchen equipment now installed in over 600 restaurants, to reach 2,000 locations by year-end.

The 27.0x exit P/E is where the repricing story is most visible. Chipotle currently trades at an LTM P/E of 29.6x and an NTM P/E near 27.0x, both already aligned with the model’s exit assumption. This means investors are paying a fair multiple today and will generate returns primarily from earnings growth rather than multiple expansion, creating a more conservative and credible setup than the headline upside suggests.

How Chipotle’s Earnings Stack Up Against CAVA and Yum Brands

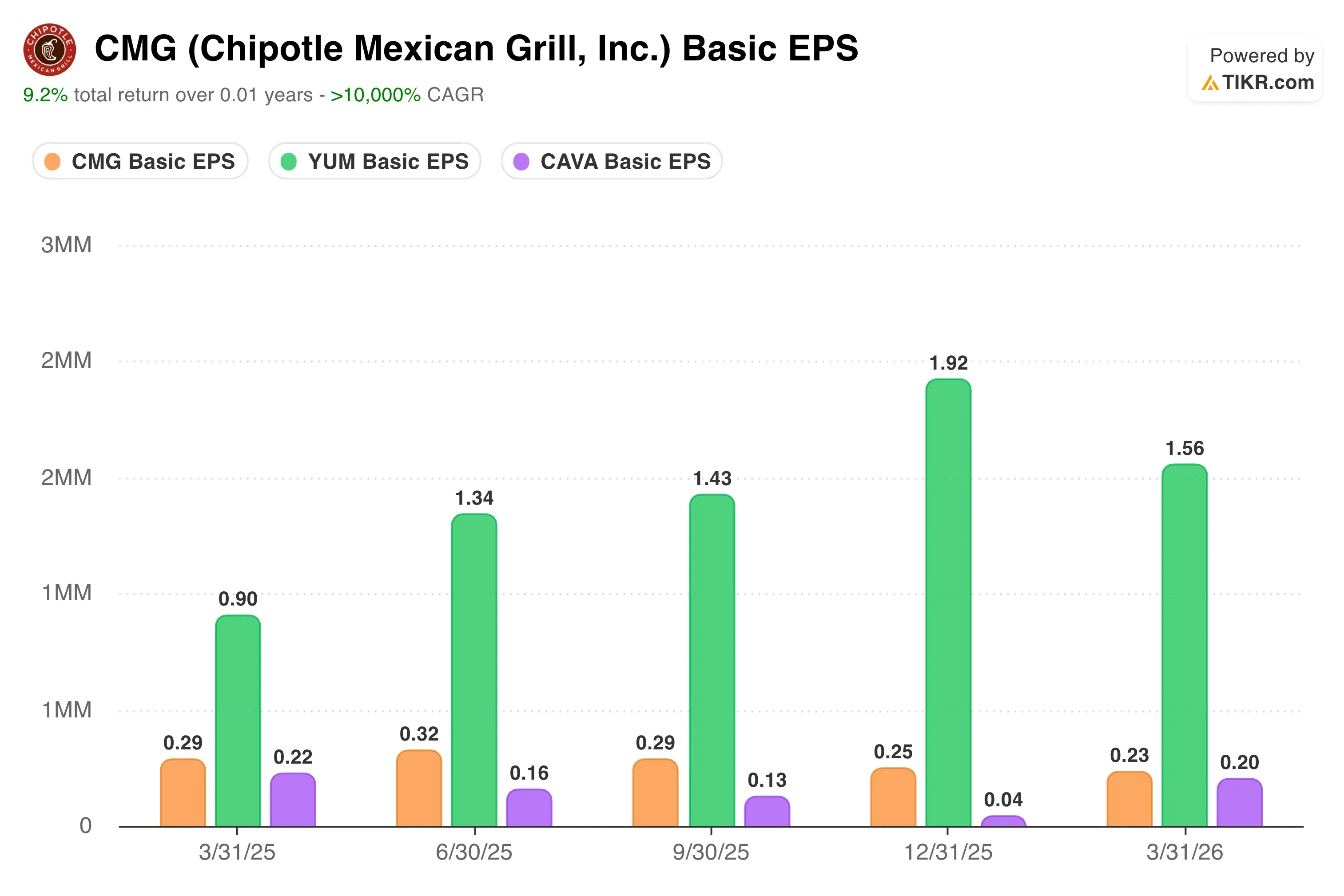

Chipotle’s GAAP diluted EPS came in at $0.23 in Q1 2026, down 17.9% year over year, while adjusted EPS landed at $0.24, also down 17.2%. Those declines reflect a business where revenue is still growing, but cost inflation is outpacing it for now. Higher labor costs, rising beef prices, and elevated effective tax rates all compressed per-share earnings even as the top line grew 7.4%.

CMG Basic EPS vs CAVA and YUM (TIKR)

CMG Basic EPS vs CAVA and YUM (TIKR)

CAVA Group (CAVA) has been growing earnings at a significantly faster pace, driven by accelerating same-store sales and a younger unit base with higher average volumes. CAVA does not yet have the earnings base to make a meaningful P/E comparison, but its trajectory is moving in the opposite direction from Chipotle’s right now, which explains the valuation premium the market assigns it.

Yum Brands (YUM) offers a more grounded EPS comparison. Yum’s adjusted EPS has been growing in the high single digits, supported by its international franchise model, which is far less exposed to U.S. labor cost inflation than Chipotle’s company-owned structure. Yum trades at roughly 22x forward earnings, so investors are paying less per dollar of earnings for a business with a more stable cost structure and global diversification.

What’s Driving CMG Stock Going Forward?

Chipotle’s most important forward catalyst is Q2 2026 comparable sales, due July 29. Management held the full-year outlook for flat comparable sales, but CFO Adam Rymer acknowledged the guidance is conservative. CEO Boatwright’s operational focus on portion consistency and value perception is aimed directly at reversing the negative traffic trend, and the return to positive 0.5% comps in Q1 after a negative Q4 is the first sign that the effort is gaining traction.

New restaurant development is the other lever that works regardless of comparable sales trends. The company plans to open 350 to 370 new locations in 2026, primarily in the U.S. but with a growing international pipeline that now includes the U.K., France, Germany, and the Middle East. Each new Chipotle in a new market carries higher first-year average unit volumes than maturing units, which makes expansion a reliable earnings growth engine even when existing store traffic is under pressure.

Technology investments will also matter over the 2.5-year model period. High-efficiency kitchen equipment, which is showing 200 to 400 basis points of comparable sales outperformance at installed locations, is expected in 2,000 restaurants by year-end.

Digital sales already represent 38.6% of total revenue, and loyalty penetration reached 32% of sales in Q1, up 300 basis points year over year. Together, those investments support throughput and margin improvement without requiring significant additional headcount.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Chipotle Mexican Grill?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CMG, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track CMG alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze CMG stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

Publishers must review books with Quranic and hadis content carefully, says Jakim

Binance Kurucusu CZ, Bitcoin ve Altcoinlerdeki Düşüşün Sebebini Açıkladı

Iraq arrests politicians and government officials in anti-corruption crackdown