General Electric Stock Is Up 45% in the Past Year. Here’s What a $210 Billion Backlog Means

Key Stats for GE Stock

- Past week’s performance: +2.1

- 52-week range: $243 to $380

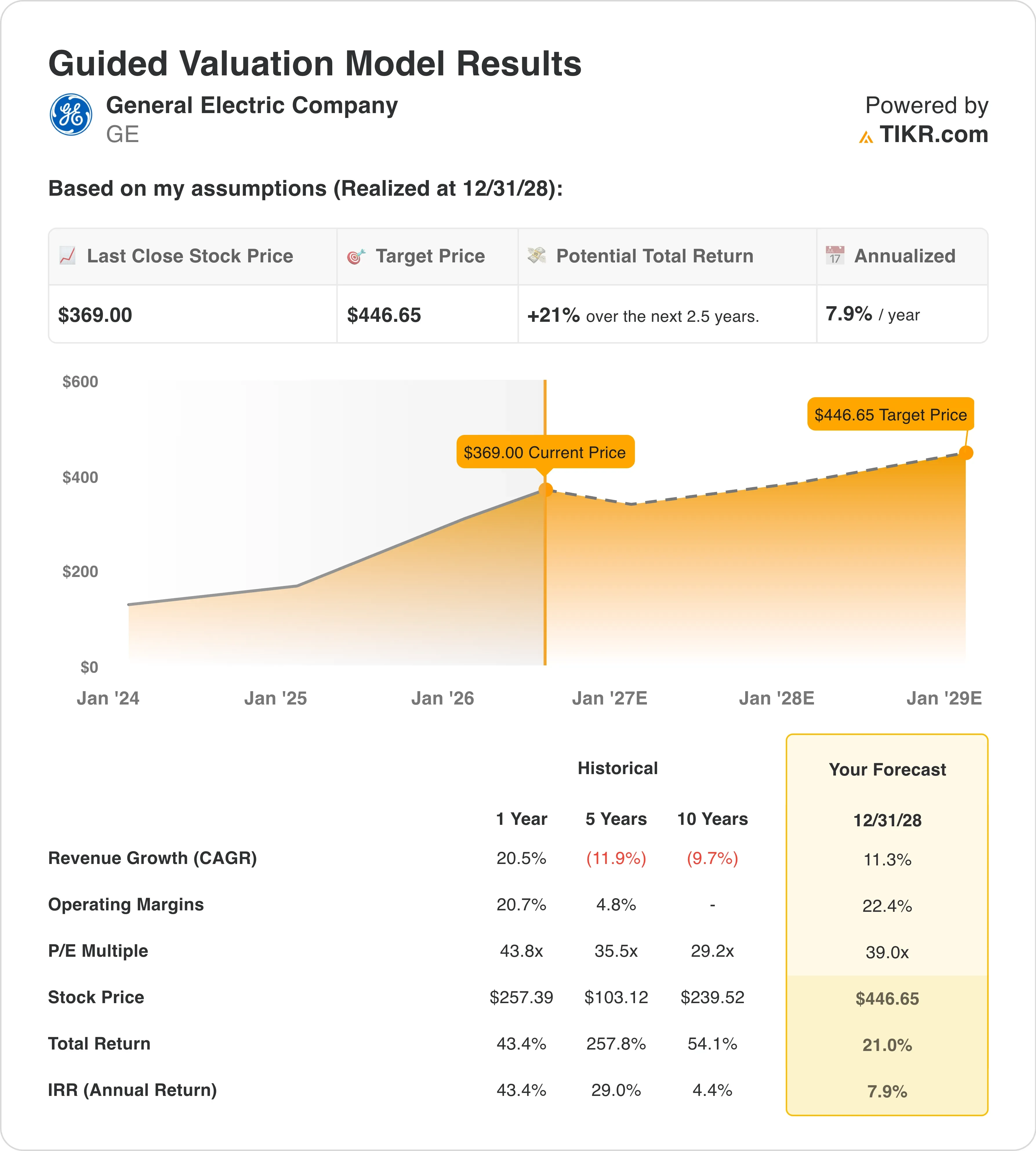

- Valuation model target price: $447

- Implied upside: 21% over the next 2.5 years

Build your own General Electric valuation scenario on TIKR (It’s free) >>>

A Q1 Beat, a $210 Billion Backlog, and Airlines Still Spending on Engines

General Electric (GE) reported a strong first quarter on April 21. Adjusted EPS jumped 25% to $1.86, beating the consensus estimate of $1.60. Revenue climbed 25% to $12.4 billion. Management followed the result by stating the company was trending toward the high end of its full-year guidance range. That kind of tone sets a constructive backdrop for months. Yet the stock gave back some gains immediately after the print, because investors were wrestling with a macro complication: elevated jet fuel prices driven by the Iran war.

GE Revenues (TIKR)

GE Revenues (TIKR)

The fuel cost story matters for GE’s customers more than for GE itself. Higher fuel costs squeeze airline margins, raising questions about whether carriers will continue ordering and overhauling jet engines at the current pace. CEO Larry Culp addressed this directly at the Bernstein Strategic Decisions Conference in late May. He told investors that airlines were still spending on engine upkeep despite the fuel spike, because grounding aircraft is more expensive than servicing them. That commentary reinforced the durability of GE’s services business, which carries higher margins than new engine sales and anchors the $210 billion backlog Culp cited in the same presentation.

Defense added fresh contract wins through May and June. GE won a three-year T700 engine support contract for the UK Apache AH-64E fleet and secured an order to power U.S. Navy Explorer-class ocean surveillance ships. These contracts are smaller in dollar terms than the commercial engine book, but they signal consistent government demand at a time when defense budgets globally are expanding. This week also brought a dividend confirmation at $0.47 per share for the coming quarter, reinforcing GE’s capital-return story alongside its operational momentum.

Going forward, GE stock will be watched closely for the Q2 earnings report on July 16. Investors will want to see whether the “trending toward the high end” commentary translates into an actual guidance raise and whether services demand held firm through the summer fuel spike.

See analysts’ growth forecasts and price targets for GE (It’s free) >>>

Is GE Stock Undervalued?

GE Guided Valuation Model (TIKR)

GE Guided Valuation Model (TIKR)

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue Growth (CAGR): 11.3%

- Operating Margins: 22.4%

- Exit P/E Multiple: 39.0x

Based on these inputs, the model estimates a target price of $447, implying 21% total upside from the current share price of $369 and an annualized return of 7.9% over the next 2.5 years.

A 7.9% annualized return sits below the 10% threshold that typically defines an attractive setup. That does not mean the story is broken. It means the market has already priced in a significant portion of GE’s post-spinoff earnings recovery. The NTM P/E of 47.6x and LTM P/E of 45.8x are elevated relative to industrial peers. GE trades at a premium because investors are paying for the earnings trajectory, not the current earnings level.

GE Guided Valuation Model (TIKR)

GE Guided Valuation Model (TIKR)

The 11.3% revenue CAGR assumption is reasonable given GE’s 1-year historical revenue growth of 20.5%. The deceleration reflects the base effect of prior engine deliveries and softer near-term commercial air traffic growth from the fuel shock. The 22.4% operating margin target compares to the current LTM EBIT margin of 20.3%, implying continued but modest improvement. The 39.0x exit P/E is aggressive by historical standards and assumes GE sustains its premium multiple as the earnings recovery matures.

However, the street target of $351 sits below the current share price, which is an unusual setup. It suggests sell-side models have not fully reflected the “high end of guidance” narrative from Q1, or that analysts are applying more conservative margin assumptions than the base case above. Either way, GE is not obviously cheap at $369. It is a quality compounder, but the margin of safety for new buyers is thin at current levels.

See General Electric’s full analyst estimate history and revenue projections on TIKR >>>

How GE Compares to Safran and Pratt and Whitney in the Engine Market

GE does not operate its commercial engine business alone. CFM International, its 50-50 joint venture with France’s Safran, is the world’s largest commercial jet engine maker by deliveries. Safran (SAF) reported stronger-than-expected Q1 jet engine revenue in April, confirming that demand at the CFM level remains robust even as individual airline margins tighten. Safran’s operating margin is recovering toward the mid-teens, while GE’s blended LTM EBIT margin is already above 20%, reflecting the higher-margin services mix that dominates GE’s revenue after the GE Vernova energy spinoff.

GE % Operating Margins vs. SAF vs. RTX (TIKR)

GE % Operating Margins vs. SAF vs. RTX (TIKR)

RTX Corporation’s (RTX) Pratt and Whitney division is the most direct competitor for new commercial engine contracts, particularly on narrow-body aircraft. Pratt is currently managing GTF engine durability issues that have grounded hundreds of Airbus A320neo aircraft. GTF stands for geared turbofan, an engine design that uses a gearbox to allow the fan and low-pressure turbine to spin at different speeds to improve fuel efficiency. The grounded fleet requires accelerated maintenance, generating service revenue even while new deliveries are constrained.

GE’s LEAP engine, delivered through CFM, does not carry the same powder-metal disk issue weighing on Pratt. That competitive distinction is one reason GE’s services backlog has grown faster in recent quarters. Airline chiefs at the IATA summit in June called out engine delays as a pressing industry-wide problem, and Pratt is more directly in the crossfire of that criticism than GE. The competitive contrast helps explain why GE commands the higher margin profile today.

Find out what’s keeping GE’s upside case alive after a 47% run >>>

What’s Driving GE Stock Going Forward?

The Q2 earnings report on July 16 is the next major catalyst. Investors will want to see whether management converts the “high end of guidance” language into an actual raised forecast for the full year. Revenue consensus for FY26 implies roughly 10% to 12% growth, consistent with the model’s 11.3% CAGR assumption. Any outperformance in services revenue, which carries GE’s highest margins, would be the most direct positive driver for the stock.

The China opportunity is an emerging wildcard. GE sees potential for more China deals following the Trump-Xi meeting in May, and Boeing’s announcement of 200 aircraft ordered by Chinese carriers creates a downstream engine demand signal. GE powers Boeing’s 737 MAX through CFM, so any increase in Chinese 737 deliveries translates directly into LEAP engine volume. Export-license uncertainty remains a risk on this front, but the diplomatic signals from May were more constructive than the prior environment.

The hybrid-electric engine program adds a long-duration option for investors thinking beyond the current cycle. GE completed a ground test of a megawatt-class hybrid electric engine system under NASA’s EPFD program in June. This is not a near-term revenue driver, but it positions GE as a credible participant in next-generation propulsion development. That matters for long-term contract relationships with both commercial and defense customers planning fleet transitions into the 2030s.

Defense budget tailwinds provide a durable offset to any softness in commercial aviation. The Pentagon’s proposed $1.5 trillion defense budget includes major line items for aircraft and engine programs GE supports.

GE’s F404, F414, and GE9X engines power multiple U.S. and allied military platforms. Combined with the Navy surveillance ship order and the UK Apache contract, GE’s defense revenue provides meaningful insulation from any near-term commercial slowdown driven by elevated fuel costs. The $0.47 quarterly dividend and a 17.7% payout ratio also leave ample room for continued capital returns as earnings grow over the next several years.

Model your own General Electric earnings scenario for Q2 and beyond on TIKR >>>

Should You Invest in General Electric?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up GE, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track GE alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze GE stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

Stakestone (STO) Soars: Token Surpasses $1.14 After Stunning 367% Rally

Bitcoin, Gold, and U.S. Stocks Dive as Trump Pledges to Hit Iran ‘Extremely Hard’