Must Read

BUSINESS DISTRICT. The skyline of Bonifacio Global City.BUSINESS DISTRICT. The skyline of Bonifacio Global City.

[Vantage Point] Ayala Land’s ‘hold’ rating: When markets blur cycles with decline

이 콘텐츠에 대한 의견이나 우려 사항이 있으시면 crypto.news@mexc.com으로 연락주시기 바랍니다

A sharp downgrade from First Metro Securities brings to the fore a host of questions concerning Ayala Land’s slowing residential business, rising debt maturities, and negative free cash flow. But does dealing with a difficult property cycle and the threat of MSCI exclusion truly justify treating one of the Philippines’ premier real estate franchises as a structurally impaired business?

My forensic read of Ayala Land’s financials is that the market may be confusing cyclical headwinds with permanent decline—and in doing so, may be undervaluing the long-term earning power of the country’s largest property developer.

Markets tend to get most optimistic near the top of a cycle and most pessimistic near the bottom. I have learned this through nearly three decades of being a financial writer and an investor.

First Metro Securities’ decision to slash its target price on Ayala Land Inc. by nearly 45% and downgrade the stock to “hold” differs from my forensic read. The report does raise legitimate concerns about slowing residential sales, debt maturities, negative free cash flow, and the possibility of removal from the MSCI Philippines Standard Index. Pencil pushing on the same numbers gives me a different conclusion.

Whether Ayala Land faces headwinds is not the main question. It does.

But do those headwinds warrant treating one of the country’s best-performing real estate franchises as a structurally impaired business? The evidence suggests otherwise.

Looking through Ayala Land’s latest financial results, we can see a company that has generated P190.2 billion in revenues in 2025 and P39.1 billion reported net income, an increase of 39% year-on-year. Even after removing one-off gains, core net income grew 8% to P30.6 billion. Those are not the numbers of a company in distress.

Ayala Land earnings in 2025 compared to 2024 (right column). Image from PSE website

Ayala Land earnings in 2025 compared to 2024 (right column). Image from PSE website

Free cash flow

The bears will argue that earnings are backward-looking and that cash flow tells a much more troubling story. They refer to a free cash flow deficit that has grown in the last few years, and about P74 billion in debt maturing over the next 12 months.

I do not dismiss those concerns. They deserve serious consideration. But context matters. I have come to believe that negative free cash flow does not mean value destruction. In real estate development, free cash flow is usually negative when you acquire land, fund construction, and expand operations. The crucial measure of success, especially for investors, is whether these upfront capital outlays build productive assets that will generate sustained earnings in the long-term.

Ayala Land’s balance sheet reveals P1 trillion in assets accumulating through decades of stringently planned development. These are not imaginary holdings. They comprise townships, commercial hubs, industrial complexes, offices, hotels, and residential centers that represent some of the most valuable real estate investments in the country.

The debt profile also seems far less alarming than First Metro Securities’ latest commentary would imply. A financially secure company—boasting P1 trillion in assets, P325 billion in equity, and constant access to local capital markets—operates in an entirely different world than one experiencing real liquidity pressure. The fact that Ayala Land has chosen to scale back its 2026 capital spending to around P50 billion is far more sobering for me, and is the mark of conservatism in an otherwise challenging period.

JCR ‘A’ rating

One thing that has been overlooked by the market is the recent reaffirmation of Ayala Corporation’s A- credit rating by the Japan Credit Rating Agency, which cited the group’s diversified earnings base, stable cash-flow generation, and balance-sheet strength.

The rating does not remove Ayala Land’s problems, but provides an independent assessment that the broader Ayala ecosystem remains financially resilient. That is important because Ayala Land constitutes one of the cornerstones of the Ayala Group.

The reaffirmation strengthens the difference between cyclical weakness and structural impairment. Slower residential sales may warrant caution, but don’t necessarily justify deeming one of the nation’s leading property franchises a financially weakened business.

That does not mean the challenges are imaginary. Residential development remains Ayala Land’s largest earnings contributor.

Headwinds

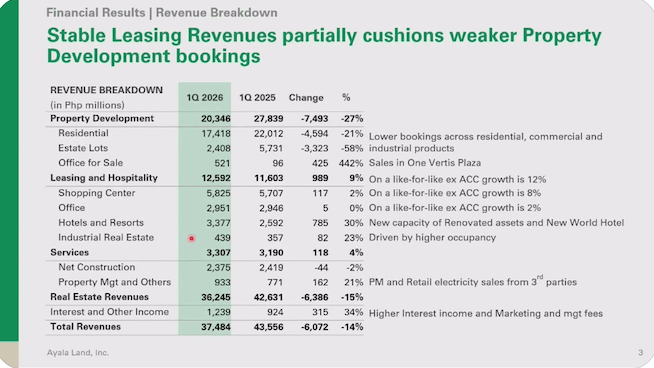

Rising interest rates, lower affordability, and slower inventory turnover have affected demand across the industry. This reality was illustrated by first-quarter 2026 results, which showed revenues falling to P37.5 billion and net income declining to P5.4 billion. (See earnings graphs below.) Property development revenues fell 27% year-on-year. Those numbers warrant consideration. What I’m missing from the bearish narrative, though, is the acknowledgment that Ayala Land is no longer simply a residential developer.

Screenshot from Ayala Land Analyst Briefing on April 30, 2026

Screenshot from Ayala Land Analyst Briefing on April 30, 2026  Screenshot from Ayala Land Analyst Briefing on April 30, 2026

Screenshot from Ayala Land Analyst Briefing on April 30, 2026

In the past two decades, the company has shifted its identity as a diversified property platform. Malls, offices, hotels, industrial parks, logistics facilities, and mixed-use townships now account for a large portion of the business. These recurring-income assets keep producing cash flow even as condominium sales slow. It’s exactly that diversification that draws me towards cautioning against the current residential weakness being perceived as a threat to the franchise itself.

MSCI deletion

I argue that the most controversial part of the downgrade is the stress on a possible removal from the MSCI Philippines Standard Index. I understand the concern. Index exclusions can spark passive-fund selling, reduce liquidity, and pressure valuation multiples. Those effects are real. But investors sometimes mistake stock-market events for business events. MSCI doesn’t build townships. MSCI does not collect rent. MSCI does not determine occupancy rates. MSCI does not generate cash flow. (READ: [Vantage Point] The uncomfortable math behind Jollibee’s MSCI demotion)

An index deletion may affect how a stock trades. It does not alter the economics of the Makati Business District, Bonifacio Global City, Nuvali, Vermosa, Arca South, or the dozens of developments that continue to generate value for Ayala Land.

Bearish thesis less convincing

For me, valuation is where the bearish thesis becomes least convincing. At recent prices of around P13 to P14 per share, the market is valuing Ayala Land at roughly 0.6 times book value. Investors are assigning a substantial discount to a company that controls nearly P1 trillion in assets and remains one of the dominant property platforms in the Philippines.

Could the stock fall further in the near term? Absolutely. A weak property cycle, elevated interest rates, geopolitical uncertainties, and possible MSCI-related selling could continue to pressure sentiment over the coming quarters. Markets rarely reward patience immediately.

But long-term investing isn’t forecasting the next quarter. It’s about determining whether the current price accurately reflects earning potential moving forward. Judging from that, Ayala Land currently appears more appealing than current sentiment suggests.

My assessment is straightforward. The near-term outlook remains challenging. There may be some time for residential demand to remain weak. Still, the long-term investment case holds true. The company has premier assets, a diversified income base, one of the strongest brands in Philippine real estate, and a balance sheet that remains far from distress, despite the pressures.

First Metro Securities may well be right about the next 12 months. But I’m less focused on the next 12 months than in the next decade. Great franchises don’t often take just 12 months to build. In my experience, they are seldom wiped out in a year, either. What Ayala Land is facing today are phase-driven or cyclical market downturns. I am convinced that the company’s underlying business model is robust enough to thrive beyond these temporary setbacks. – Rappler.com

Click here for more Vantage Point articles.

시장 기회

Blur 가격(BLUR)

$0.01789

$0.01789$0.01789

USD

Blur (BLUR) 실시간 가격 차트

면책 조항: 본 사이트에 재게시된 글들은 공개 플랫폼에서 가져온 것으로 정보 제공 목적으로만 제공됩니다. 이는 반드시 MEXC의 견해를 반영하는 것은 아닙니다. 모든 권리는 원저자에게 있습니다. 제3자의 권리를 침해하는 콘텐츠가 있다고 판단될 경우, crypto.news@mexc.com으로 연락하여 삭제 요청을 해주시기 바랍니다. MEXC는 콘텐츠의 정확성, 완전성 또는 시의적절성에 대해 어떠한 보증도 하지 않으며, 제공된 정보에 기반하여 취해진 어떠한 조치에 대해서도 책임을 지지 않습니다. 본 콘텐츠는 금융, 법률 또는 기타 전문적인 조언을 구성하지 않으며, MEXC의 추천이나 보증으로 간주되어서는 안 됩니다.

추천 콘텐츠

ETS back on track after power outage, but eight services running late

KUALA LUMPUR, June 14 — Repair works following the overhead line equipment (ATA) outage at KM 458.872 between Tiro...

공유하기

Malaymail2026/06/14 19:03

EdgeX (EDGE) Rallies 15.2% to ATH as Volume Surges $57M: Data Analysis

EdgeX (EDGE) reached a new all-time high of $0.784 on April 2, 2026, marking a 15.2% single-day surge. Our analysis of on-chain metrics and market structure reveals

공유하기

Blockchainmagazine2026/04/03 07:03

Perplexity AI Predicts Shocking Solana Price in 6 Months

Perplexity AI did not come here to be cautious. Its 6 month predicts on Solana lands at a base... The post Perplexity AI Predicts Shocking Solana Price in 6 Months

공유하기

ICO Bench2026/06/14 19:12

인기 뉴스

더보기