NKE Is Down 50% From Its Peak. Here’s What the Numbers Say Now.

Key Stats for Nike Stock

- 52-Week Range: $40.44 to $80.17

- Current Price: $40.90

- Street Mean Target: $58.13

- Market Cap: ~$60.6B

- LTM Gross Margin: 40.9%

- LTM EBIT Margin: 6.7%

- Dividend Yield: 4.4%

- NTM P/E: 25x

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Gross Margin Has Fallen 3 Points Since 2022

Nike (NKE) has not lost its identity as the Swoosh still commands prime shelf space at every major retailer, the Jordan brand remains one of the most valuable in footwear, and no competitor has matched the company’s global athlete roster or marketing reach. What Nike has lost, at least for now, is the profitability that justified its premium valuation.

Gross margin peaked at 45.98% in fiscal 2022, then began compressing as Nike leaned too heavily into its direct-to-consumer digital channel, pulled back from wholesale partners, and found itself stuck with excess inventory. By fiscal 2025, gross margin had declined to 42.73%. The most recent quarter came in at 40.2%, as tariffs in North America added another layer of cost pressure.

Nike Gross Margins. (TIKR)

Nike Gross Margins. (TIKR)

CEO Elliott Hill, who came out of retirement to take the top job in October 2024, has been transparent about the scope of the reset. The company is rebuilding wholesale relationships it let atrophy, clearing promotional inventory, and refocusing product development on athletic performance rather than lifestyle.

Hill has described the initiative as “Win Now,” though analysts are increasingly noting that the timeline looks more like “Win Eventually.” RBC, for example, recently pushed its expectations for meaningful revenue recovery out to 2027.

See the exact moment Wall Street upgrades NIKE stock before the rest of the market piles in — track analyst rating changes in real time with TIKR for free →

Revenue Flat, Earnings Down 45%, and Q4 Still Ahead

Nike reports fiscal Q4 results on June 30, and the setup is not easy. Management has guided for low-single-digit revenue declines through the end of calendar 2026, with Greater China expected to fall around 20% as the company deliberately reduces sell-in to clean up marketplace inventory. Converse, the wholly-owned subsidiary that sells canvas sneakers and lifestyle footwear, fell 35% in Q3 to $264 million and remains a significant drag.

North America is the brightest spot. Wholesale revenues grew 5% in Q3 on a reported basis, suggesting that the channel rebuild with retail partners is gaining traction. That is meaningful progress, but it has not been enough to offset weakness elsewhere.

There is also a CFO transition underway. Nike announced this week that Matthew Friend will step down, replaced by David Denton, formerly CFO of Pfizer and Lowe’s, effective August 17. Jefferies analyst Randall Konik framed the move as a signal that Hill is installing the right operators for a multi-year reset. Citi was more cautious, flagging the timing as a surprise given the proximity to both Q4 earnings and a planned fall analyst day.

Nike EPS Normalized. (TIKR)

Nike EPS Normalized. (TIKR)

Normalized EPS has reflected the full weight of the reset. Earnings fell from $3.95 in fiscal 2024 to $2.16 in fiscal 2025. Consensus estimates project a further decline to around $1.50 in fiscal 2026, followed by a gradual recovery. The Street sees earnings rebuilding toward roughly $4.70 by fiscal 2030, essentially a return to Nike’s level before the contraction began.

Track the Q4 results and the trajectory of Nike stock’s North America momentum ahead of the June 30 earnings call on TIKR for free →

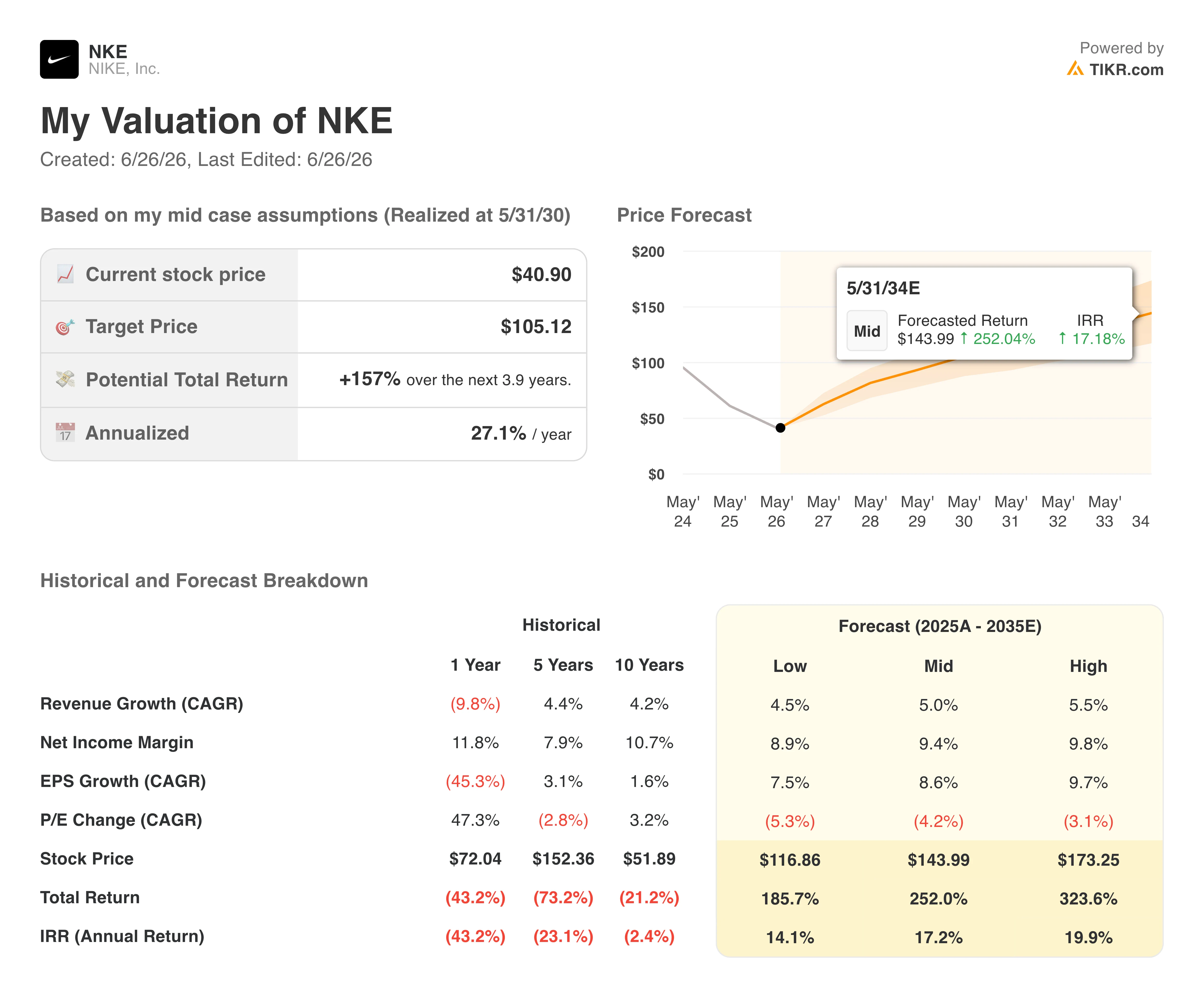

The Model Sees 157% Upside. Here’s What It Requires.

TIKR’s valuation model targets around $105 for Nike stock in the mid case, assuming roughly 5% annual revenue growth and net income margins recovering to around 9% over the next several years. That scenario implies a potential total return of around 157% over approximately four years, or about 27% annualized.

The wide range across scenarios is worth noting. The low case produces around $117, while the high case reaches around $173, both measured at fiscal year 2030. The spread reflects genuine uncertainty about how quickly margins will recover and whether P/E multiple compression will continue as earnings rebuild.

TIKR’s model also shows the historical context: even the low case implies a return to profitability well above Nike’s current level.

Nike Valuation Model. (TIKR)

Nike Valuation Model. (TIKR)

The central question for Nike investors is not whether the brand survives. It is whether the current price already compensates for years of below-average earnings ahead, and whether Hill’s operational reset translates into the durable margin recovery the model requires.

Should You Invest in Nike, Inc.?

Nike is a genuine turnaround story at a genuinely depressed price.

The brand is intact, the balance sheet carries manageable debt, and the dividend has grown for 24 consecutive years. The recovery case is real. But the timeline keeps slipping, margins are still under pressure from tariffs and the DTC unwind, and Greater China remains a meaningful headwind with no clear resolution in sight.

Investors buying today are essentially betting that Hill’s operational reset works, that wholesale momentum in North America continues, and that earnings trough in fiscal 2026 before a multi-year rebuild takes hold. If those pieces fall into place, the upside is substantial. If the recovery takes longer than the model assumes, the wait could be long.

Pull the full TIKR model for NKE, including EBITDA estimates through 2030, on TIKR for free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

2 rentung nahas di DUKE

Has Bitcoin Finally Bottomed? Realized Price Theory Points to More Downside Ahead

James Carville predicts next GOP candidate turns on Trump from surprising direction