Grant Cardone’s Real-Estate Bitcoin Loop: Can Property Cash Flow Become a New BTC Treasury Model?

Real-estate cash flow buying Bitcoin sounds like internet myth until you see the receipts. Grant Cardone is actually doing it, wiring rental income into BTC on a steady schedule and structuring hybrid funds that hold both apartments and coins. This piece breaks down how that loop works, who it might fit, and what could break if you try to copy it.

We will keep it practical. Mechanics first, then accounting, risk, and where this sits next to just holding a spot ETF. Along the way, we will point to the latest moves and what they signal for corporate treasuries eyeing Bitcoin.

Quick Answer

Yes, property cash flow can fund a Bitcoin treasury, but it only makes sense inside a clear mandate, with patient capital, and with risk controls you can actually execute. Cardone Capital has proven the loop is doable by dollar cost averaging BTC with rental income and pairing assets inside hybrid vehicles. It is not plug and play for every landlord or CFO, and the risk sits on both sides of the balance sheet.

- Mechanism: use net operating cash flow to DCA BTC on a set cadence rather than lump-sum bets.

- Why now: hybrid real-estate plus BTC funds are live and scaling, including Cardone Capital’s approach reported in June 2026.

- Big risks: BTC volatility, liquidity timing for property ops, and governance limits in fund documents.

- Who it fits: sponsors with recurring cash flow, long horizons, and LPs who opt in to a mixed-mandate strategy.

- Alternatives: spot ETF exposure, traditional corporate treasuries, or nothing at all if mandates are tight.

How does the property-to-Bitcoin loop actually work?

The basic engine is simple. Instead of distributing 100 percent of free cash flow or letting it idle in cash, the sponsor routes a slice of recurring rental income into scheduled Bitcoin buys. Cardone Capital publicly framed this as a dollar cost averaging program and, as of late June, held roughly 200 million dollars in BTC while managing about 5.3 billion dollars in AUM, with a stated target return band of 22 to 32 percent for the hybrid funds CoinDesk.

On the ground, that looks like periodic purchases funded by stabilized assets. Cardone even posted that the firm added 282 BTC on June 19, 2026, roughly 18 million dollars at mid-June prices, tying the buy to ongoing cash generation rather than one-off capital raises Crypto.news.

There is also a pairing design that matches specific properties with a defined BTC allocation inside a single product. One example cited in mid-June 2026: a 366-unit Boca Raton asset reportedly purchased for 235 million dollars paired with a 100 million dollar BTC bucket within the fund structure Bitcoin Magazine. The pairing makes the exposure explicit, so LPs know they are buying both a building and coins.

In other words, the loop is not just vibes or tweets. It is a treasury policy that takes recurring operating income and points it at BTC according to rules in the offering docs, then reports performance across two engines: rents and Bitcoin.

What separates this from a classic corporate BTC treasury?

Most corporate treasuries that touch Bitcoin either hold spot directly, use a spot ETF, or do nothing and keep the float in short-term paper. High profile outliers have also used debt or equity proceeds to buy BTC. The Cardone approach is different because the buying power comes from a real operating flywheel that keeps spinning through cycles and because it is presented as an integrated product to LPs rather than a surprise treasury bet.

To position it clearly, here is a quick comparison of common BTC treasury paths alongside the property cash flow loop.

Strategy Funding source Volatility tolerance Liquidity profile Governance friction Who it fits Property cash flow DCA (Cardone-like) Recurring NOI allocations Moderate to high, long horizon Low near-term liquidity unless BTC sold High if docs are not explicit, lower if opt-in Real-estate sponsors with stable assets and aligned LPs Debt or equity financed buy Capital markets raises High, given leverage and market risk Depends on treasury policy and loan covenants High, board and lender approvals Public companies with conviction and access to capital Direct spot on balance sheet Existing cash reserves Low to moderate, often capped BTC is liquid, but sales can be sensitive Medium, audit and policy updates required Cash-generative firms diversifying treasury Spot Bitcoin ETF Existing cash reserves Low to moderate High, tradable hours with market liquidity Low, simple ops and custody outsourced Conservative treasuries and boards

One more piece of context: corporate and public treasuries are already moving. A June dataset tallied about 51,000 BTC added or disclosed in May 2026, net 43,500 after reductions, with public company holdings rising above 1.2 million BTC by month end. That backdrop shows treasury adoption is not a one-off idea BitcoinTreasuries.net. Cardone’s twist is the funding source and product design.

Could a REIT or private real-estate fund copy this in 2026?

Private funds probably can, if they write it into the mandate and the LPs sign off. Hybrid structures that pair property with BTC exposure are already in market, and the mechanics are straightforward if you have stabilized cash flow and a custody setup that auditors accept.

Public REITs face more constraints. Many are bound by investment policies focused on real property and related assets, and they operate under distribution requirements and leverage covenants that can clash with a BTC sidecar. A board could potentially approve a small allocation or use a spot ETF in a taxable subsidiary, but that is a legal and tax question that needs bespoke counsel. Even then, investor relations risk is real if income investors expect boring dividends, not coin price swings.

For private sponsors, the cleanest path is the opt-in hybrid: disclose the target BTC slice, how it is funded, custody and audit approach, and how the sponsor will treat cash needs if BTC sells off. If you are trying to retrofit an existing fund midstream, expect heavier LP consent mechanics and maybe a separate vehicle to avoid mixing mandates.

Where are the risks hiding and how do you hedge them?

There are two big buckets: market risk and liquidity timing. Bitcoin can move 10 percent in a day. Property can be slow to sell, slow to refinance, and occasionally needs sudden capital. If the portfolio takes a maintenance hit the same quarter BTC is down 30 percent, you do not want to be a forced seller of coins at the bottom just to fix a roof or fund reserves.

Hedges are mostly policy and process. Think hard position limits, a ring-fenced reserve for property ops, cadence rules you can pause, and collateral lines that do not use BTC if the loan covenants could turn procyclical. Some sponsors will keep BTC unencumbered and free of lending programs to avoid collateral calls.

Operational risk matters too. Custody, key management, auditor comfort, and cyber posture are not paperwork. If your SOC reports and key ceremonies are weak, you are taking enterprise risk that has nothing to do with price. And yes, this all has to tie out under your fund docs and compliance program.

How do accounting and taxes tilt the decision in 2026?

Accounting has quietly become more accommodating. Under updated US GAAP, most companies now carry crypto assets at fair value with changes in earnings for fiscal years starting after late 2024, with early adoption permitted. In 2026, that means many treasuries can reflect both upside and downside in a cleaner way than the old impairment-only model. It removes the headache of writing down and never writing up, though it does put P&L swings in your face.

For funds, you still need to square how NAV is struck and how distribution waterfalls treat BTC gains and losses. Some hybrid vehicles may track performance sleeves so that property cash flow metrics remain transparent. Talk to your auditor about presentation and disclosures before the first buy. It is not a place to wing it at year end.

Taxes will vary by jurisdiction and entity type. Corporates may face standard capital asset treatment for BTC, while REITs have tighter rules on what counts as good income and qualified assets. Using a taxable REIT subsidiary or alternative structure might be necessary if a public REIT wants exposure at all. Private funds generally have more room, but cross-border LPs, UBTI concerns for certain investors, and withholding rules can complicate things. Get a memo in writing.

What should boards and LPs measure to keep this honest?

Do not let Bitcoin become a vibes-only line item. Treat it like any other engine with KPIs and guardrails. Here is a simple checklist teams actually use:

- Allocation targets and hard caps by vehicle, with a board-level max.

- Cash buffer rules for property operations, stress-tested for 12 to 24 months.

- Buy cadence logic and pause triggers tied to liquidity, not to price predictions.

- Custody controls: key management, whitelists, insurance, and dual approvals.

- Reporting: sleeve-level performance, look-through risk, and scenario tables.

- Exit plan: rules for trimming, rebalancing, and how proceeds are treated.

To help with context, track what the broader market is doing. Aggregate treasury additions in May 2026 were reported at 51,000 BTC gross and 43,500 net, with public company holdings above 1.2 million BTC BitcoinTreasuries.net. If your board wants to know whether they are out on a limb, that is the benchmark set.

Is this worth it now, or is a spot ETF simpler?

Depends what you want. The Cardone-style loop is about turning a steady, lower-volatility asset into a pair trade: durable rent checks funding a volatile asset with asymmetric upside. You get potential outperformance at the cost of a choppier P&L and more operational work.

The spot ETF route is simpler, faster, and likely easier to pass through governance. You still get Bitcoin exposure, just without the integrated story of cash flow funding coins. In practice, a lot of boards will prefer the ETF because it avoids custody heavy lifting and because it is easy to trim or exit without touching operating cash.

If you can credibly run property ops and a coin treasury, the hybrid can be compelling. Cardone’s live examples - including the Boca Raton pairing and the 282 BTC DCA buy - show you can do this in size Bitcoin Magazine Crypto.news. But for most treasuries, the first step is a policy-approved ETF sleeve while you study what it takes to own spot directly.

Who should not try this, even if they love Bitcoin?

If your properties are early in lease-up, highly levered, or need heavy capex, you probably need every free dollar to de-risk the asset. If your LP base signed up for pure-play real estate and has zero appetite for coin volatility, changing the rules mid-game is a fast way to lose trust.

On the corporate side, if your cash flows are seasonal or your working capital swings are large, you do not want BTC competing with payroll or vendor payments. Realize that a Bitcoin treasury is a cultural commitment. If leadership will panic-sell at the first drawdown, do not start.

Common Mistakes

- Mixing liquidity pools. Using BTC as the primary backstop for property opex sets you up to sell bottoms. Keep a separate cash reserve for buildings.

- Buying before governance is ready. If the mandate is not explicit, you invite LP disputes and audit friction. Amend docs first, then buy.

- Chasing price with cadence changes. DCA only works if you stick to it. Constantly tweaking buy sizes based on headlines ruins the edge.

- Custody shortcuts. Skipping key policies, insurance discussions, or auditor-approved workflows turns treasury into operational risk.

- Leverage on leverage. Borrowing against properties to buy BTC, then lending out BTC, stacks risks. Keep it unencumbered unless you are built for liquidations.

If you want ongoing coverage, analysis, and the occasional nudge to check your assumptions, you can always find the latest markets perspective at Crypto Daily.

Frequently Asked Questions

Can LPs opt into the Bitcoin sleeve without touching the real estate?

In some structures, yes. Sponsors can run parallel vehicles - one pure property, one hybrid - or create a sleeve structure where LPs choose their allocation at subscription. It depends on the legal setup and transferability rules.

Does DCA timing matter if Bitcoin is so volatile anyway?

DCA is about process, not prediction. The edge is reducing timing luck and keeping buys small enough that no single entry matters. It will not save you from a full-cycle drawdown, but it usually beats sporadic lump-sum buying.

What happens if BTC rallies hard and becomes a big chunk of NAV?

Have a rebalance rule. Some sponsors cap BTC at a percentage of NAV and trim back on strength, redeploying gains to property reserves or distributions. Decide this before the rally, not after.

Is there any signaling benefit for fundraising?

Maybe. Some LPs like seeing conviction and alignment with macro themes. Others will walk. The real benefit is clarity - if your thesis is a two-engine portfolio, make it explicit and let the market self-select.

Could a lender punish me for holding BTC on the side?

It is possible. Some loan covenants and relationship banks are conservative about non-core assets. Keep the BTC vehicle structurally separate and disclose as needed so it does not contaminate property-level tests.

How big should the BTC slice be to matter?

There is no universal number, but single digit percentages of NAV are a common starting range in treasury contexts. Enough to move the needle over time, small enough to survive a full drawdown without crippling ops.

Why not just mine Bitcoin instead?

Mining is a completely different business with capex cycles, energy strategies, and hash price risk. If you are a landlord or CFO, a treasury allocation is usually cleaner than standing up an industrial operation you do not know how to run.

Disclaimer: This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.

You May Also Like

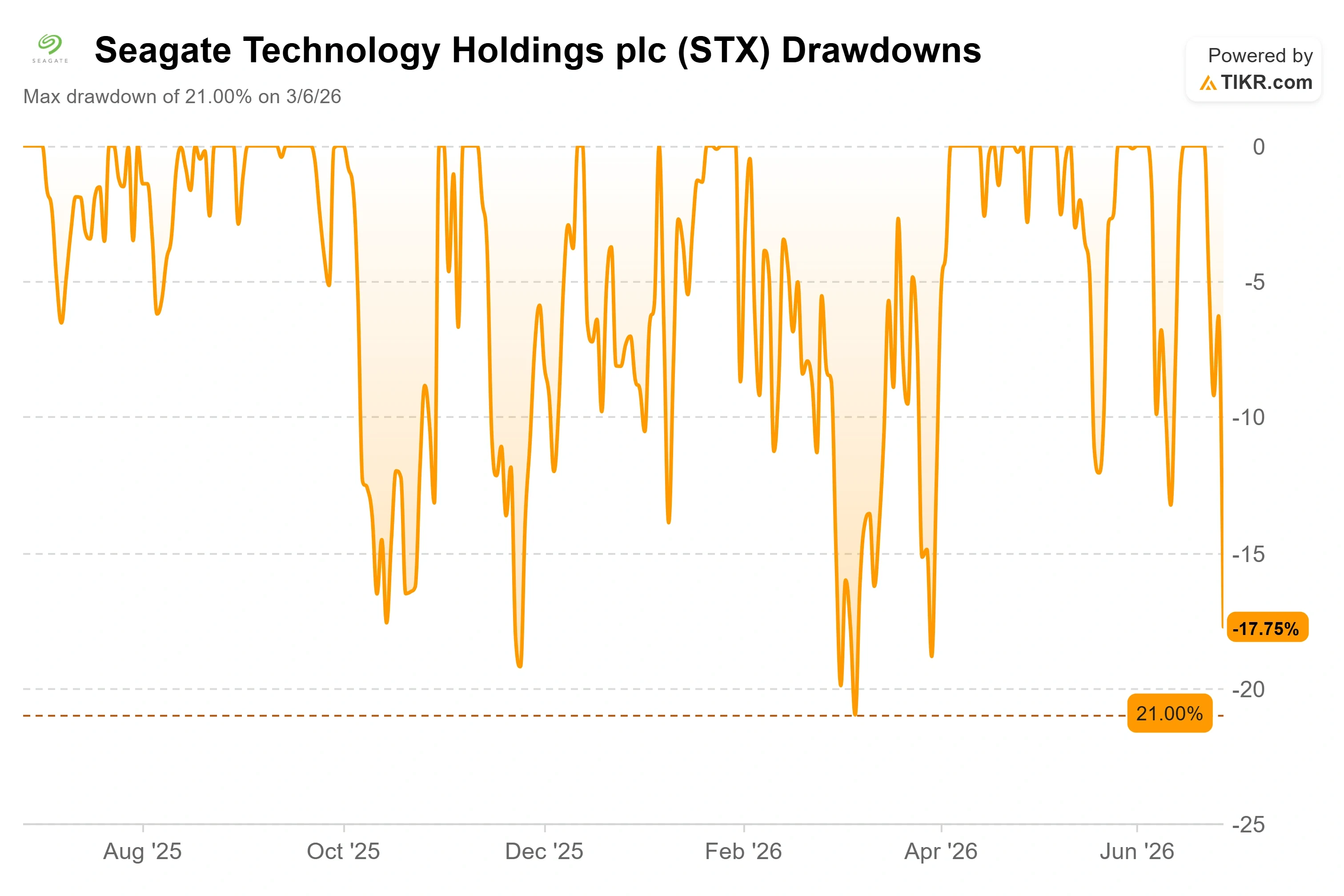

Seagate Stock Fell 12% in a Day. Here’s Where the Stock Could Go in 2026

George Conway and Mehdi Hasan deliver searing indictment of 'dumb' Trump’s presidency

BitMine Just 500K ETH Away From 5% Supply Goal