Why Monolithic Power Systems Stock Could Be Worth $2,453 on AI Demand

Key Takeaways for Monolithic Power Systems Stock as of June 2026

- Analysts rate Monolithic Power Systems stock 11 buys, 2 holds, and 1 underperform, with a mean target of $1,789, implying around 36% upside from the current price of $1,313.

- TIKR’s mid-case model values Monolithic Power Systems at around $2,453 by December 2030, implying around 87% total return, or roughly 15% annualized.

- Management guided Q2 2026 revenue of $890 million to $910 million, roughly 11% above the prior Street consensus of $816 million.

MPWR beat estimates and raised guidance by double digits in a single quarter. See if the valuation catches up to the fundamentals on TIKR for free →

MPWR Stock Delivers Record Q1 Revenue and Raises Enterprise Data Growth Floor to 85%

Monolithic Power Systems (MPWR) reported record Q1 2026 revenue of $804.2 million on April 30, up 26.1% year over year and above the prior Street consensus of $781 million, as AI infrastructure demand accelerated across two of its fastest-growing segments.

Monolithic Power designs power management semiconductors that regulate voltage and improve energy efficiency in AI servers, data centers, automotive systems, and optical networking hardware.

Enterprise Data revenue more than doubled year over year to $262.8 million in Q1 2026, driven by higher sales of power management solutions for AI accelerators and server applications.

Communications revenue grew 33% sequentially in Q1 2026, fueled by power solutions for 800-gigabit optical modules and top-of-rack switches, segments where MPS competes on power density inside physically constrained module enclosures.

VP of Finance Tony Balow raised the company’s Enterprise Data outlook sharply on the Q1 earnings call: “The strong ordering patterns that we saw start last year has kind of continued through Q1. So at this point in time, I think we’re comfortable raising that floor up to around 85% year-over-year growth.”

That revision moves the Enterprise Data growth floor from 50% to 85% year over year, a step-change driven by extended customer ordering patterns and improved backlog visibility across both AI accelerator and server CPU applications.

MPS also won complete dismissal of a patent infringement lawsuit filed by Bel Power Solutions in U.S. District Court, with the court granting summary judgment of non-infringement on all asserted claims and Bel Power agreeing to pay MPS court costs of $50,000.

The company set a new near-term manufacturing capacity target of $6 billion, up from the original $4 billion plan, with supply chain infrastructure spread both inside and outside China to manage geopolitical risk.

MPS reported Q1 2026 adjusted EPS of $5.10, beating the Street estimate of $4.90, while EBIT reached $288 million against a consensus estimate of $276 million, with EBIT margins widening to 35.8% year over year.

For Q2 2026, management guided revenue of $890 million to $910 million, representing roughly 12% sequential growth and landing around 11% above the prior analyst consensus of $816 million.

MPS just raised its Enterprise Data growth floor by 35 percentage points in a single quarter. Model the full revenue trajectory on TIKR for free →

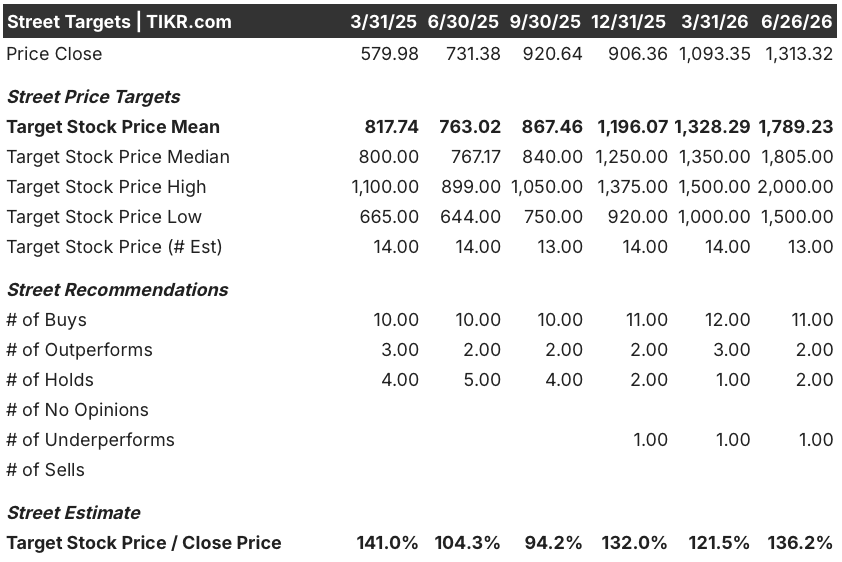

Wall Street Holds 11 Buys on Monolithic Power Systems Stock with a $1,789 Mean Target

Thirteen analysts cover Monolithic Power Systems stock as of June 26, 2026, with 11 buys, 2 holds, and 1 underperform rating on record.

The mean price target stands at $1,789, implying around 36% upside from the June 26 close of $1,313.

The current mean target of $1,789 represents a significant step up from the $1,328 mean recorded at the end of Q1 2026, reflecting upward revisions following the Q1 earnings beat and Q2 guidance raise.

Street Analysts Target for MPWR Stock (TIKR)

Street Analysts Target for MPWR Stock (TIKR)

Wall Street Expects Monolithic Power Systems Stock Revenue to Accelerate Past 33% in Q2 2026

MPWR Stock Revenue Actuals & Estimates (TIKR)

MPWR Stock Revenue Actuals & Estimates (TIKR)

Analysts expect MPS to report Q2 2026 revenue of around $900 million, consistent with the midpoint of management’s guidance range of $890 million to $910 million, representing roughly 36% growth year over year.

Monolithic Power Systems stock appears to be undervalued at current levels, with the revenue acceleration from $804 million in Q1 to an expected $900 million in Q2 supported by a backlog-driven 85% Enterprise Data growth floor that the Street had not fully modeled before April 30.

The forward revenue curve remains steep: estimates project Q3 2026 revenue of around $980 million, rising to around $1.01 billion in Q4, representing roughly 33% and roughly 35% year-over-year growth respectively.

The unresolved condition the Street watches is whether Communications segment momentum, up 33% sequentially in Q1, extends through the second half of 2026 as 800-gigabit optical module volumes continue to ramp.

TIKR’s $2,453 Target on MPWR Stock Holds as Enterprise Data Floor Removes the Key Bear Case

TIKR’s mid-case model values Monolithic Power Systems at around $2,453 by December 2030, implying around 87% total return from the current price of $1,313, or roughly 15% annualized over 4.5 years.

MPWR Stock Valuation Model Results (TIKR)

MPWR Stock Valuation Model Results (TIKR)

A roughly 15% annualized return positions MPWR stock well above the typical 8% to 10% annual return expectation for large-cap semiconductor holdings, reflecting the company’s above-sector revenue growth trajectory.

The target is reachable because management removed the primary bear case, replacing a 50% Enterprise Data growth floor with an 85% floor backed by extended ordering patterns and improved backlog visibility, while Q2 guidance of $890 million to $910 million came in around 11% above prior Street consensus, confirming the acceleration is already in the order book.

TIKR’s mid-case puts MPWR at around $2,453 by December 2030. Build your own valuation model on TIKR for free →

Should You Invest in Monolithic Power Systems, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Monolithic Power Systems stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Monolithic Power Systems stock alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze MPWR stock on TIKR for Free →

You May Also Like

Inside CryptoKaleo’s Recent Commentary — What It Means for Traders

Michael Burry Just Bet Big Microsoft Will More Than Double by 2028

‘I’ll listen to ‘Only the Young’ at home on my own’: Zohran doesn’t know about a Swift-Kelce wedding at MSG, but he’s not going