Snowflake Broke Out to $249 as the AI Data Thesis Reignites. Here’s Where the Stock Could Go in 2026

Key Stats for Snowflake Stock

- Current Price: $248.96

- Target Price (Mid): ~$705

- Street Target: ~$293

- Potential Total Return: ~183%

- Annualized IRR: ~25% / year

- Earnings Reaction: +36.48% (May 27, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Snowflake Inc. (SNOW) closed Friday at $248.96, up 9.65% in a single session, and the move was not noise. The stock had spent the entire week pinned between $225 and $230, the kind of tight range that usually breaks hard in one direction. It broke up, on heavy volume, in what traders described as a clean upside breakout rather than a reaction to any single headline. What investors rallied around was a thesis, not a press release: the growing belief that Snowflake is becoming the default place enterprises run their AI data.

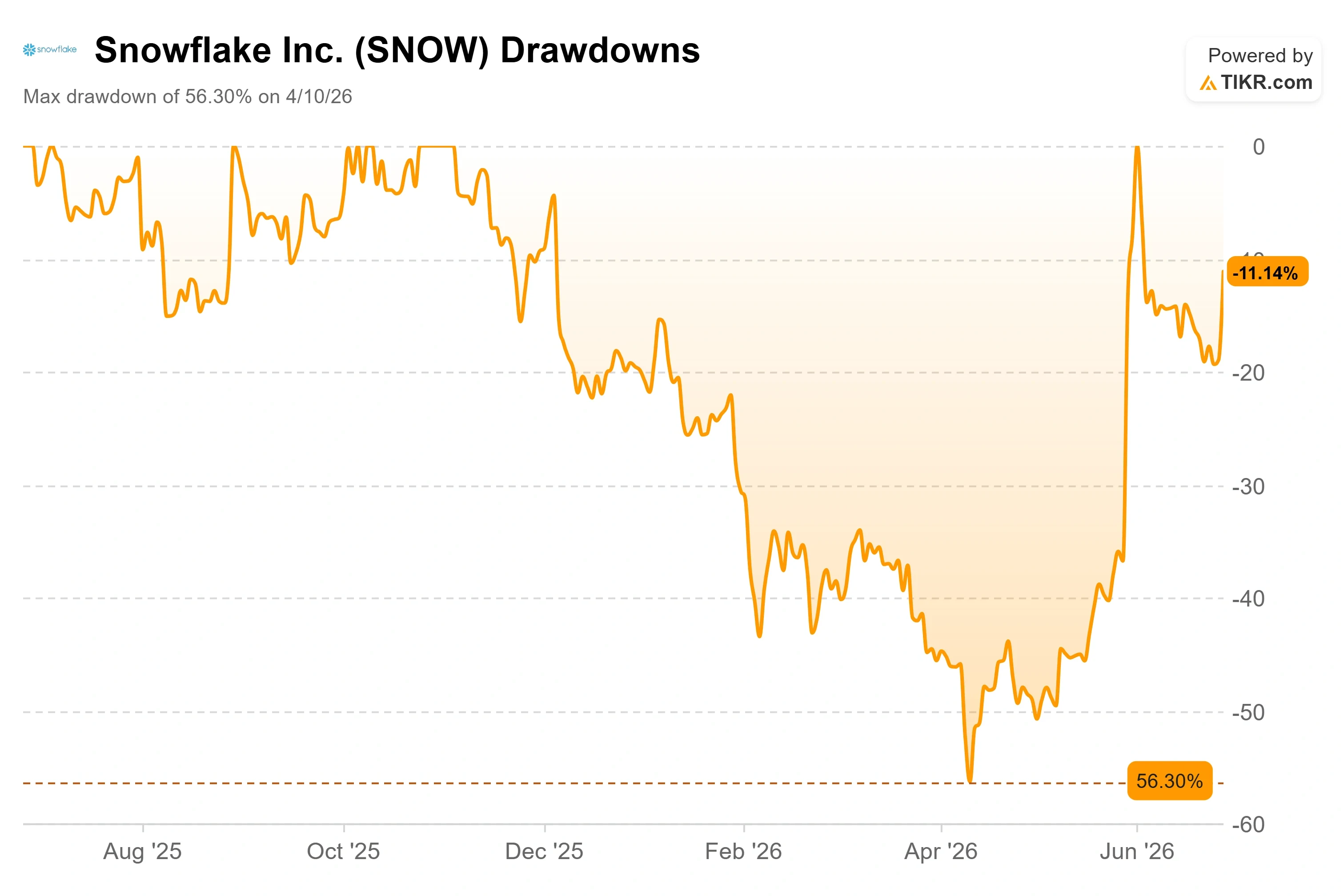

For most of 2026, the SNOW debate was about damage. The stock cratered 56% from its high to a low of $118.30 on April 10, then nearly doubled off that floor. Friday’s pop means it is now up roughly 51% in just the past month. The question has flipped. It is no longer “is the business broken.” It is “after a run like that, is there anything left.” That tension, between a stock that has already moved a lot and a thesis that may only be getting started, is the whole story right now.

The Unlimitail Win Is the Narrative Bulls Are Anchoring To

The proof point fueling the bull case is Unlimitail, a retail media network spanning Europe and Latin America that, on June 17, selected Snowflake to power its upcoming Global Retail Media Data Hub. Retail media, meaning the business of retailers selling ad space and targeting it with their own shopper data, is one of the fastest-growing corners of advertising. Unlimitail’s network reaches 250 million shoppers across more than 35 retail partners, including Carrefour and MediaMarkt Saturn. The hub will run on Snowflake Data Clean Rooms, a secure setup where brands and retailers combine data without ever exposing raw customer records to each other.

The reason this matters is what it proves. Snowflake’s pitch is that the differentiation in AI is not the model, it is the data. A marquee customer building an entire industry hub on Snowflake’s collaboration stack is exactly the real-world signal bulls have been waiting for. As Simon Contreras, Industry Principal for Retail and Consumer Goods at Snowflake, said in the company’s announcement, “Most retail media measurement stops at the click. With Unlimitail, brands can go all the way to the receipt.” That last-mile measurement, tying ad spend to actual purchases, is the feature retailers will pay to consume, and consumption is how Snowflake makes money.

Snowflake Drawdowns (TIKR)

Snowflake Drawdowns (TIKR)

See historical and forward estimates for Snowflake stock (It’s free!) >>>

The Bigger Shift Happened on June 2

The breakout sits on top of something more structural. At its Investor Day on June 2, held alongside the Snowflake Summit, management did something it had never done before: it put a date on profitability. The company committed to reaching GAAP profitability in the fourth quarter of fiscal 2028 and raised its full-year non-GAAP operating margin guidance to 13.5%, more than double the 6.4% it delivered in fiscal 2025.

CFO Brian Robins was specific about how. The plan leans on two levers, operating expense and stock-based compensation, with stock-based comp falling from 41% of revenue toward 27%. He was blunt about the discipline behind it, saying the company is “being extremely disciplined on headcount,” and noting that net headcount grew by just 17 in one recent quarter as Snowflake used its own AI tools to do more without hiring. CEO Sridhar Ramaswamy framed why that matters: “It isn’t clear that simply throwing more humans at problems gets more things done.” For a company that spent years defending growth at any cost, a credible, dated profitability promise changes the kind of investor who can own it.

What the Bulls and Bears Are Actually Fighting About

The bull case is consumption reacceleration. Product revenue grew 34% year over year last quarter, up from 30% the quarter before and 26% a year ago, and net revenue retention climbed back to 126%. The engine is Cortex Code, the AI coding agent Snowflake calls CoCo internally, which Ramaswamy says “sells itself” into the company’s existing base of roughly 14,000 customers. His logic is simple: “Everything you do with Snowflake is going to be 10x faster. They’d be foolish to not go try it out.”

The bear case is valuation and credibility. SNOW trades at around 73x NTM EV/EBITDA, meaning enterprise value against next twelve months’ expected earnings before interest, taxes, depreciation and amortization, a multiple that demands flawless execution. The insider signal is also uncomfortable: director and former CEO Frank Slootman sold roughly $46.8 million in stock across recent transactions, part of more than $343 million in insider selling over the past 90 days. When a former chief executive sells into strength, some investors read it as informed sellers taking the run off the table. A separate overhang remains the securities class action covering alleged misstatements from June 2023 through February 2024, a known legal risk that predates the current rally and remains unresolved.

There is also a competitive question that the market keeps circling. One analyst at Investor Day pointed out that Snowflake’s low-30s revenue growth trails a primary competitor growing nearly twice as fast. Ramaswamy did not dodge it, replying simply, “I don’t know what to say. Absolutely.” Robins added that the company’s guidance is “based on rooted observed behavior,” meaning Snowflake will only raise its outlook as usage actually shows up. That candor is either reassuring or alarming, depending on which side of the trade you are on.

Where Snowflake Sits Against Its Peers

On the valuation multiples that matter for software, Snowflake is in a class of its own, and not in a flattering way. It trades at around 13.1x NTM revenue against IBM at roughly 4.3x, the only directly comparable name with populated peer figures on TIKR’s IT Services list. On NTM EV/EBITDA, Snowflake sits near 73.6x versus IBM’s 15.3x. That premium is enormous. Whether it is justified comes down to one variable: growth durability. IBM grows in the low single digits. Snowflake is compounding revenue above 30% with a forward two-year revenue CAGR estimated near 28%. The market is paying up for a growth rate IBM cannot touch, so the premium is defensible only as long as that gap holds.

Snowflake Product Operating Revenue (TIKR)

Snowflake Product Operating Revenue (TIKR)

See how Snowflake performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $248.96

- Target Price (Mid): ~$705

- Potential Total Return: ~183%

- Annualized IRR: ~25% / year

Snowflake Advanced Valuation Models (TIKR)

Snowflake Advanced Valuation Models (TIKR)

See analysts’ growth forecasts and price targets for Snowflake stock (It’s free!) >>>

This analysis uses the TIKR Valuation Model mid-case, realized on January 31, 2031. That case targets a price of around $705, implying roughly 183% total return over about 4.6 years, or around 25% annualized.

The two revenue drivers are continued enterprise AI workload migration onto Cortex AI and CoCo, and deepening consumption among Snowflake’s largest customers, where the top 25 accounts now average $34 million in annual spend, up from $22 million two years ago. The margin driver is operating leverage as stock-based compensation falls from 41% of revenue toward 27%, lifting net income margins toward the mid-case 14.4%. The primary risk is competitive displacement from faster-growing AI-native data platforms, which the consumption model would translate directly into slower revenue.

The upside is that CoCo consumption and wins like Unlimitail keep product growth above 30% while margins inflect, validating the multiple. The downside is that a single quarter of decelerating consumption, in a model anchored to usage rather than committed bookings, resets a 73x EBITDA stock fast.

Conclusion

The next real test is Q2 fiscal 2027 earnings, due in late August. Watch product revenue against management’s guidance of approximately $1.42 billion, which implies roughly 30% growth. A beat that holds or lifts the 31% full-year product revenue outlook would confirm the consumption reacceleration is durable and that Friday’s breakout was the start of a new leg, not a blowoff top. A miss, or any softening of guidance, would hand the bears their proof that a 51% one-month run got ahead of the business. The Unlimitail hub itself goes live later this year, and the consumption it drives will start showing up in exactly that line. Everything in this thesis comes back to one number: does usage keep accelerating, or doesn’t it?

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Snowflake?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Snowflake, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Snowflake alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Snowflake on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

'I get it now': Anthony Scaramucci reveals epiphany he had thanks to 'not well' Trump

What Happens to the XRP Price if the Crypto Bear Market Gets Worse?

Solana SOL Reclaims $72, But Fading On-Chain Metrics Signal Weakening DEX Momentum