Comfort Systems Stock Fell 8% This Week. Here’s Where the Stock Could Go in 2026

Key Stats for Comfort Systems Stock

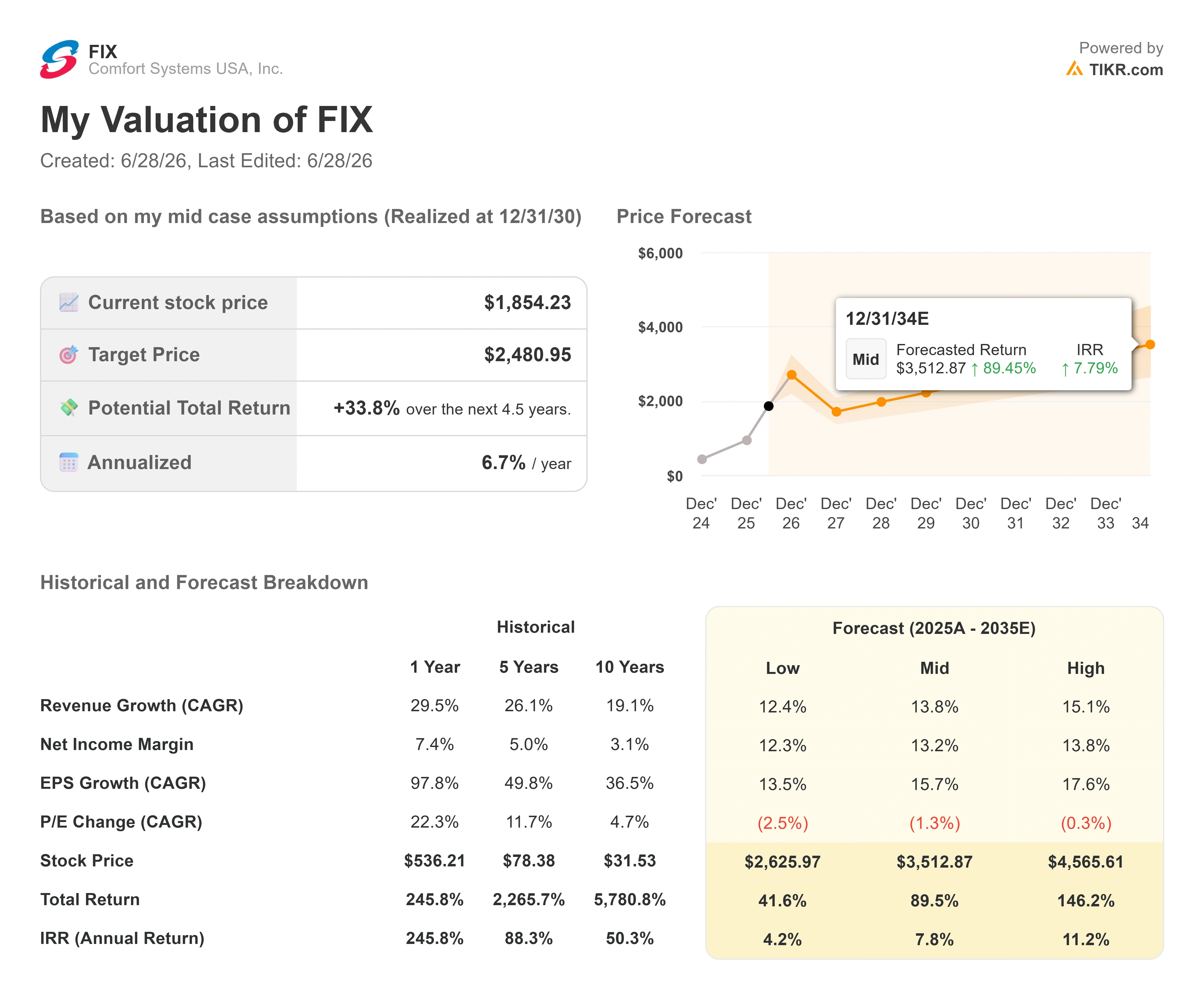

- Current Price: $1,854.23

- Target Price (Mid): ~$2,480

- Street Target: ~$2,048

- Potential Total Return: ~34%

- Annualized IRR: ~7% / year

- Earnings Reaction: -2.69% (April 24, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Comfort Systems USA (FIX) just had its worst day in months, and nothing actually broke. The stock fell 8.1% on June 26 to close at $1,854.23, capping a slide of roughly 10% from its all-time closing high of about $2,066 set only four days earlier. There was no earnings miss. No guidance cut. No lost contract. For a stock still up about 95% in 2026, that combination is exactly what makes the move worth understanding.

The tension here is real. Bulls see a mechanical contractor sitting on a record order book at the center of the AI data center build-out, with demand visibility that its own management calls unprecedented. Bears see a construction company trading near 42x forward earnings, with insiders selling into the rally and a stock that has tripled in a year. The question the market cannot yet answer is simple: was this week’s drop the first crack in an overextended winner, or a discount on one of the most visible growth stories in U.S. industrials?

What the Selloff Was Actually About

Start with what did not happen. The decline was not tied to any negative operating update. The most plausible explanation is ordinary profit-taking after a powerful run, layered on top of two specific items that gave cautious traders a reason to act.

The first is insider selling. Over the three months through late June, Comfort Systems insiders sold roughly $47 million in stock with no recorded purchases, according to research from Simply Wall St. CEO Brian Lane, who made the largest sale among them over the trailing year. Insider selling sends an ambiguous signal on its own, but clustered selling into a vertical move tends to sharpen the market’s caution.

The second is a leadership reshuffle. On June 22, after the close, Comfort Systems announced internal changes effective July 1: Craig Sasser, currently Regional Vice President for the Atlantic Region, becomes Chief Operating Officer, while Briston Blair becomes Chief Strategy and Innovation Officer. The filing read as an administrative succession, not a warning. It carried no reduction in outlook and no change to business conditions. President and COO Trent McKenna continues in his leadership role. Markets near record highs are simply primed to read any change as a reason to lighten up.

None of that touches the order book, which is where the optimism lives.

Comfort Systems Drawdowns (TIKR)

Comfort Systems Drawdowns (TIKR)

See historical and forward estimates for Comfort Systems stock (It’s free!) >>>

A Record Backlog and a Demand Curve Management Has Never Seen

Comfort Systems installs and services the mechanical, electrical, and plumbing (MEP) systems, meaning the heating, cooling, power, and water infrastructure, that keep data centers, factories, and commercial buildings running. The company exited Q1 2026 with a record backlog, its forward book of legally committed and priced contracts, of $12.5 billion.

That number frames the recent enthusiasm, and management has been blunt about the durability behind it. At the Sidoti Small-Cap Virtual Investor Conference on June 18, President and COO Trent McKenna described demand in terms he has not used before. “I’ve never seen a demand curve quite like what we’re seeing,” he told analysts, adding that he keeps expecting it to change and that “at this point, we see no change of it at all. It just continues to go out into the future.” When the operating head of a 23,000-employee contractor frames the pipeline that way, it matters because backlog conversion is the entire engine of the forward growth estimates.

The scale of the data center opportunity is easy to underestimate. Director of Investor Relations Chrissy Nelson put concrete math on it at the same conference: of the hyperscaler capital spending investors hear announced, roughly 80% goes to chips and servers, and only the remaining 20% is the physical data center build. Comfort Systems’ scope of work is about 50% to 60% of that 20%. That share, applied across the wave of announced hyperscaler spending, is what underwrites multi-year visibility rather than a single strong quarter.

Why the Quarter and the Analysts Backed the Story

The fundamentals under the backlog have been extraordinary. In Q1 2026, reported on April 23, Comfort Systems posted revenue of $2.87 billion, up 56% year over year and nearly 20% above the consensus of $2.40 billion. EPS of $10.51 more than doubled the prior-year figure and beat estimates by roughly 54%. EBITDA of $524 million came in about 50% above expectations. Despite the blowout, the stock fell 2.69% on April 24 as the market recalibrated to full-year guidance that, while strong, implied deceleration off a record comparison.

CEO Brian Lane summarized the quarter plainly in the earnings release, citing “organic revenue growth this quarter of 51% compared to the same quarter of last year, and per share earnings that have more than doubled over the same period.” Organic growth at that level matters because it shows the demand is being captured by the existing business, not just bolted on through acquisition.

Wall Street responded with conviction. On April 24, KeyBanc upgraded FIX to Overweight from Sector Weight with a $2,004 target, saying valuation had previously been the limiting factor and that it now saw a good entry point. UBS later raised its target to $2,125 from $1,992 on June 8. Of the analysts covering the stock, 7 rate it a Buy against just 1 Hold, with no sells. The current Street target sits near $2,048, still comfortably above where the stock trades after this week’s drop.

The valuation is where the debate gets honest. FIX trades around 29x NTM EV/EBITDA, a clear premium to its closest large-cap peers. Quanta Services (PWR), the nearest comparable, trades around 30x on the same basis, while EMCOR Group (EME) sits far lower at around 18x. So Comfort Systems is priced at a premium to EMCOR and roughly in line with Quanta, despite the FIX 49.7% return on invested capital (ROIC) being among the highest of any industrial company in the market. The premium is justifiable on returns and visibility, but it leaves little margin for a stumble. That is precisely why an 8% drop with no bad news still rattles the tape.

Comfort Systems Beats & Misses (TIKR)

Comfort Systems Beats & Misses (TIKR)

See how Comfort Systems performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $1,854.23

- Target Price (Mid): ~$2,480

- Potential Total Return: ~34%

- Annualized IRR: ~7% / year

Comfort Systems Advanced Valuation Model (TIKR)

Comfort Systems Advanced Valuation Model (TIKR)

See analysts’ growth forecasts and price targets for Comfort Systems stock (It’s free!) >>>

Using the TIKR mid-case scenario, realized at the end of 2030, the model points to a target of around $2,480 per share. That implies a total return of roughly 34% over about four and a half years, or an annualized IRR near 7% per year. After this week’s drop, the entry price is meaningfully below where the model’s clock started.

Two revenue drivers carry the case. The first is data center and hyperscaler MEP demand, which pushed the technology end market to about 56% of year-to-date 2026 revenue and filled the record backlog. The second is modular capacity, expanding to 4 million square feet by year-end, which lets the company pre-fabricate complex systems off-site and capture work that on-site labor constraints would otherwise cap. On margins, the swing factor is mix: higher-complexity electrical and modular work has lifted gross margin above 25%, and the mid-case assumes net income margin holding around 13%. The primary risk is multiple compressions. The model itself assumes the P/E contracts each year modestly, and any hyperscaler capital-spending pause would accelerate that.

The upside: if data center volumes hold and the modular ramp lands, revenue compounds in the mid-teens and the stock works back toward and past the Street’s $2,000-plus targets.

The downside: a capex slowdown collides with an already-premium multiple, and the same operating leverage that powered the run reverses on the way down.

Conclusion

The cleanest test arrives on July 23, when Comfort Systems reports Q2 2026. Watch gross margin. Q1’s reported margin was lifted by a one-time project closeout gain, and stripping that out puts the underlying figure around 25%. A Q2 print at or above 25% without that tailwind would confirm the margin expansion is structural rather than a function of favorable closeouts, and it would tell you this week’s selloff was about price, not the business. A drop back toward 24% or below, paired with any softening in same-store growth, would hand the bears their first piece of real evidence and put the premium multiple under genuine pressure. After an 8% drop on no news, the next earnings call stops being a victory lap and becomes the number that settles the argument.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Comfort Systems?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Comfort Systems, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Comfort Systems alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Comfort Systems on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

Why The Green Bay Packers Must Take The Cleveland Browns Seriously — As Hard As That Might Be

Luck, Stupidity, and Getting Ripped Off

Why an Altcoin Rally Could Start When Everything Still Looks Terrible