Broadcom Stock Is Down 26% From Its High. Here’s Why the OpenAI Chip Deal Changes the Custom AI Story

Key Stats for AVGO Stock

- Past week’s performance: -6.9%

- 52-week range: $263 to $495

- Valuation model target price: $470

- Implied upside: 28.8% over the next 2.3 years

Value your favorite stocks like AVGO with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

The Software Miss, the Stock Drop, and the OpenAI Deal That Followed

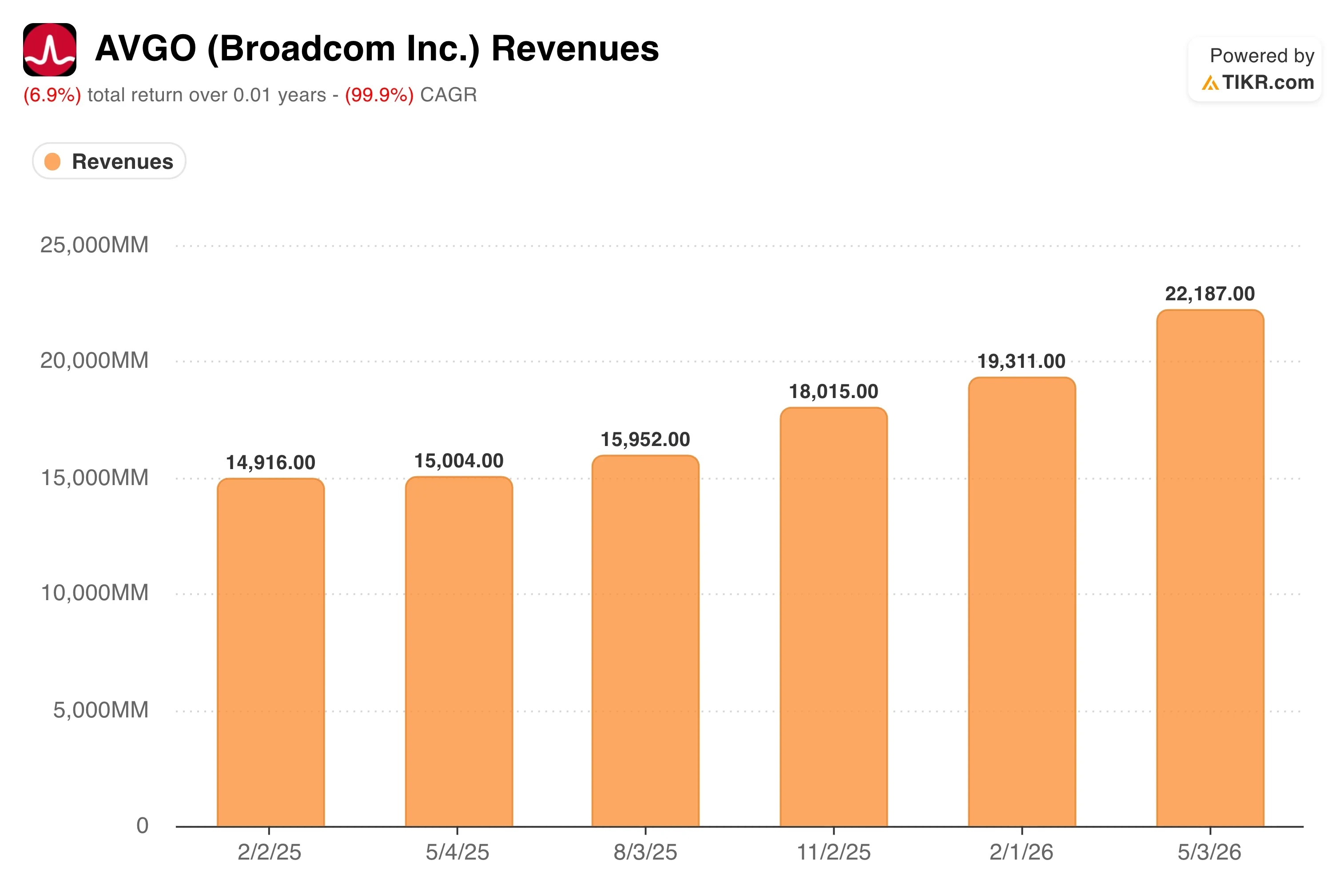

Broadcom Inc. (AVGO) entered June under heavy selling pressure. Its fiscal Q2 2026 results, reported on June 3, showed total revenue rising 48% year over year to a record $22.2 billion. AI semiconductor revenue hit a record $10.8 billion, up 143% year over year. Yet the stock fell sharply in the days that followed. The selloff had two triggers.

AVGO Revenues (TIKR)

AVGO Revenues (TIKR)

First, Broadcom’s infrastructure software division posted $7.18 billion in revenue, missing analyst expectations of $7.32 billion. Second, the Q3 AI revenue guide of $16 billion came in below some analyst estimates of $17.2 billion, even though $16 billion would still represent over 200% growth year over year.

CEO Hock Tan was direct about what is driving the AI business. “Broadcom achieved record revenue, operating profit and free cash flow in Q2 driven by accelerating growth in AI semiconductor revenue and strong operating leverage,” Tan said. “The momentum continues, and in Q3 we expect semiconductor revenue from AI to grow over 200% year-over-year to $16.0 billion.” That commentary framed the selloff as a valuation reset rather than a business deterioration. Investors who had priced in perfection were trimming positions, not changing their view of AI demand.

Then came the June 24 catalyst. OpenAI unveiled a custom chip it designed with Broadcom called the Jalapeño LLM inference chip platform. LLM stands for large language model, the type of AI that powers products like ChatGPT. Inference means running those models after they are trained, which is the highest-volume and most cost-sensitive part of AI deployment. The Jalapeño chip is designed to make inference faster and cheaper at massive scale. OpenAI plans an initial rollout by late 2026, with volume ramp-up into 2027 and 2028.

The announcement reinforced Broadcom’s position as the go-to partner for hyperscalers designing their own silicon. Earlier in June, Apollo and Blackstone backed Anthropic’s $35 billion capacity expansion in a new Broadcom-anchored AI compute platform. Going forward, AVGO stock will be watched closely as these custom chip partnerships convert from announcements into shipped revenue.

See how analysts are modeling Broadcom’s custom AI chip revenues on TIKR >>>

Is AVGO Stock Undervalued After the Selloff?

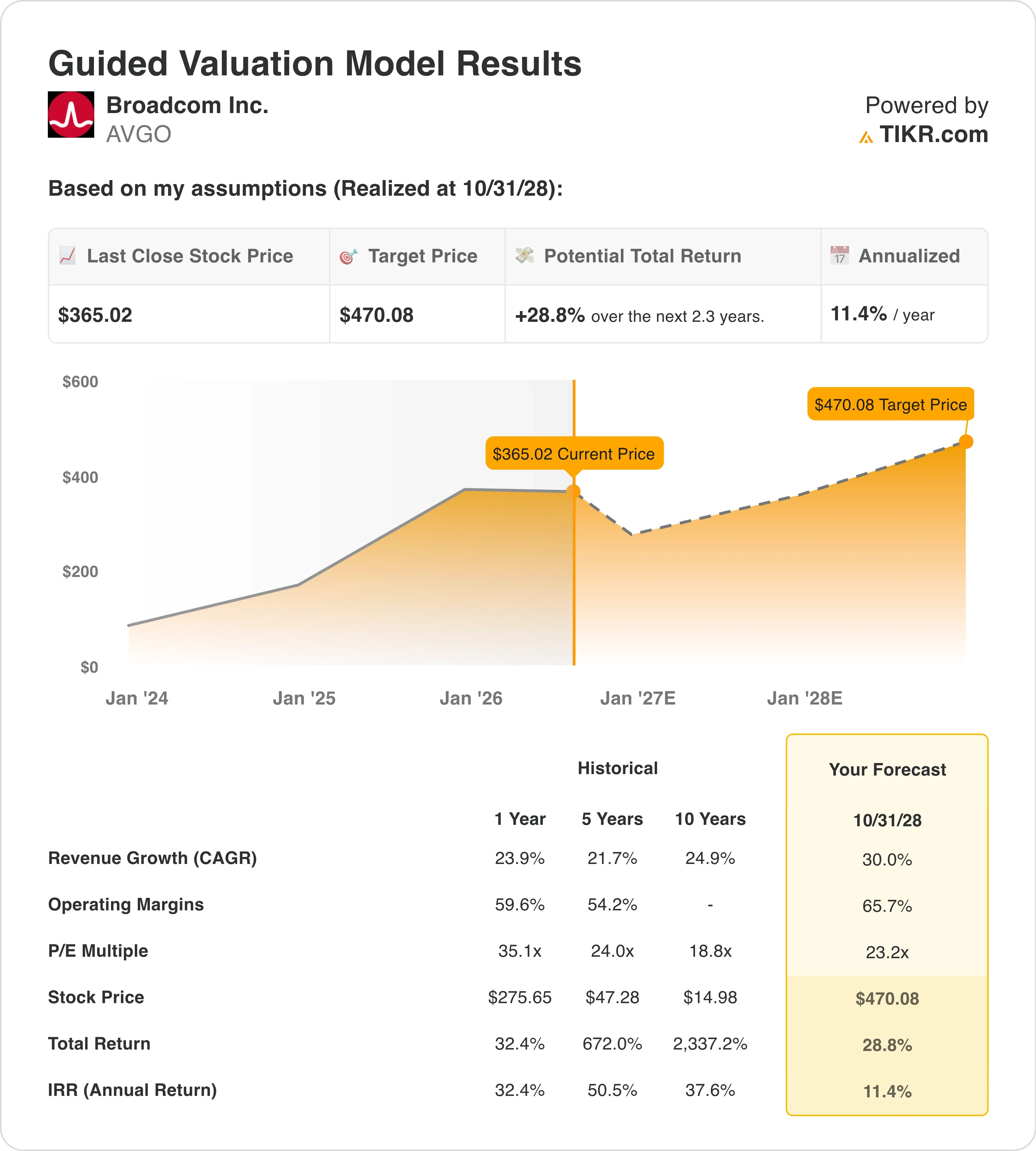

AVGO Guided Valuation Model (TIKR)

AVGO Guided Valuation Model (TIKR)

Under valuation model assumptions realized through 10/31/28, the stock is modeled using:

- Revenue Growth (CAGR): 30.0%

- Operating Margins: 65.7%

- Exit P/E Multiple: 23.2x

Based on these inputs, the model estimates a target price of $470, implying 28.8% total upside from the current share price of $365 and an annualized return of 11.4% over the next 2.3 years.

That 11.4% annualized return sits right at the threshold where a stock earns attention. It is not a screaming buy signal, but it does suggest the post-earnings selloff has compressed the multiple to a more defensible level. The stock peaked near $495 in early 2026 and now trades around $365, a drawdown of roughly 26%. At that level, the market is pricing in continued AI revenue growth but demanding that Broadcom convert its growing XPU pipeline into shipped product consistently.

AVGO NTM P/E (TIKR)

AVGO NTM P/E (TIKR)

The 30% revenue CAGR assumption is bold but grounded in recent history. Broadcom’s 1-year revenue CAGR ran at 23.9%, and its 5-year rate was 21.7%. The 30% forecast assumes the hyperscale custom silicon cycle accelerates further. The 65.7% operating margin assumption reflects confidence that the VMware software integration stays on track.

AVGO Guided Valuation Model (TIKR)

AVGO Guided Valuation Model (TIKR)

Software carries far higher margins than semiconductors, and Broadcom’s LTM EBIT margin is already 44.2%, so the expansion path implies meaningful software-mix improvement. The 23.2x exit P/E assumes continued multiple compression from today’s NTM P/E of roughly 23x, which is already well below the 35x level of a year ago. The model therefore bakes in no valuation re-rating, only earnings growth.

The implied return is above 10% annually but not dramatically so. That keeps Broadcom in the category of attractive for long-term holders. The street target of $524 implies considerably more near-term upside than the conservative base case above.

Run your own revenue and margin assumptions for Broadcom on TIKR (Free with TIKR) >>>

How Broadcom Stacks Up Against Marvell and Nvidia

The custom silicon space Broadcom dominates is not uncontested. Marvell Technology (MRVL) is the most direct comparable, also designing custom AI accelerators for cloud hyperscalers. The company sees custom chip revenue topping $10 billion by 2029, putting it on a growth trajectory similar to Broadcom’s AI segment. Marvell trades at a premium NTM P/E but carries far lower absolute revenue. Broadcom’s scale advantage, its dual-engine model combining semiconductors with VMware infrastructure software, creates a moat Marvell cannot replicate alone.

AVGO % Gross Margins vs. MRVL vs. NVDA (TIKR)

AVGO % Gross Margins vs. MRVL vs. NVDA (TIKR)

Nvidia (NVDA) operates in a different lane. It sells GPU-based training and inference clusters rather than custom ASICs tailored to a specific customer’s workload. ASIC stands for application-specific integrated circuit, meaning a chip built for one company’s exact architecture rather than a general-purpose graphics processor. Nvidia’s gross margins exceed 70%, and its revenue growth over the past two years has outpaced almost every company in the index. But the OpenAI-Broadcom Jalapeño partnership is explicitly about reducing inference costs at scale.

As frontier AI labs seek to run models more cheaply, custom ASICs become more attractive relative to renting GPU clusters. That shift does not hurt Nvidia in model training, but it does create a ceiling on GPU inference revenue growth at scale. Broadcom’s LTM gross margin of 76.3% already rivals Nvidia’s profile, and the VMware software layer adds recurring revenue that Nvidia does not have.

Find out what’s driving Broadcom’s AI upside case today (Free with TIKR) >>>

What’s Driving AVGO Stock Going Forward?

The most important near-term driver is how fast Broadcom converts its custom XPU pipeline into shipped AI revenue. CEO Hock Tan guided Q3 AI semiconductor revenue at $16 billion, which would represent over 200% year-over-year growth. That is the number investors will benchmark when Broadcom reports on September 3. Any shortfall versus that guide would likely trigger another round of selling. A beat would reopen the bull case and potentially push the stock back toward the $400 to $420 range.

The OpenAI Jalapeño chip is a medium-term revenue catalyst. The initial deployment is expected by late 2026, with volume ramp in 2027 and 2028. That timeline means revenue contribution will be modest in fiscal 2026 but potentially meaningful in fiscal 2027. OpenAI is one of the largest consumers of AI compute in the world, so even a partial share of its inference workload represents a significant revenue stream. Broadcom confirmed six core custom chip customers, including Anthropic, Google, Meta, and OpenAI, which provides a concentrated but high-conviction customer base.

The VMware integration also matters for long-term margin trajectory. LSEG renewed its Broadcom partnership with a five-year VMware Cloud Foundation deal, an example of how the software segment is converting legacy relationships into durable recurring revenue. Software margins are structurally higher than silicon margins, so every VMware renewal pushes Broadcom’s blended margin profile higher. The CFO transition, with Amie Thuener joining from Alphabet, adds an executive with direct cloud-infrastructure experience at a moment when that background is directly relevant to Broadcom’s biggest growth bets.

Finally, Broadcom upsized its cash tender offer for senior notes to $3 billion, paying down higher-cost debt. LTM net debt is $45.3 billion, but net debt to EBITDA stands at just 1.07x, which is manageable given Broadcom’s free cash flow generation. The capital structure is clean enough to support continued investment in AI partnerships and product development without straining the balance sheet.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Broadcom?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up AVGO, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track AVGO alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze AVGO stock on TIKR Free→

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

iTrading Platform Catapult Trade Partners with Binance Wallet, Confirms $PULT Token

Vitalik Buterin Proposes Self-Sovereign AI Stack To Protect Users From Risks Of AI Agents