Ethereum is splitting into three power centers and ETH treasury firms are paying for two

Ethereum Institutional announced its launch on July 1, folding a year of the Foundation's go-to-market work into a group pitching Ethereum to banks and asset managers on tokenization and stablecoins.

Ethlabs, built by five former senior Ethereum Foundation (EF) researchers, surfaced days earlier with the goal of faster settlement and ETH's monetary case. Bitmine, Sharplink, and Joe Lubin fund both initiatives.

The timing lines up with an organizational unraveling within the Foundation itself, as Hsiao-Wei Wang stepped down as EF co-executive director on June 18, joining Tomasz Stańczak's earlier resignation and at least eight senior departures over five months.

The Foundation's own March 2026 mandate already redefined its role: as a steward of self-sovereignty, censorship resistance, open-source code, privacy, and security, with no claim to being Ethereum's parent or final authority.

That leaves room, deliberately or not, for outside groups to take over the commercial half of the work.

Ethlabs absorbed the technical and asset-value side, focused on infrastructure readiness, ETH as a monetary instrument, and the arguments that make institutions comfortable holding and building on the chain.

Ethereum Institutional absorbed the sales side through relationship-building, forums, and the pitch decks that turn interest into deployed capital.

Both moved outside the EF because the Foundation was never built to run either function well. A neutral standards body cannot double as ETH's advocacy shop or a corporate sales team without diluting the credibility that makes it useful as a standards body in the first place.

The Foundation holds legitimacy and long-term protocol values, Ethlabs holds ETH value capture and technical readiness, and Ethereum Institutional holds corporate distribution.

| Function | Old center | New emerging center | Strategic meaning |

|---|---|---|---|

| Values, neutrality, protocol legitimacy | Ethereum Foundation | Still Ethereum Foundation | EF preserves Ethereum’s credible-neutrality layer. |

| ETH value capture and infrastructure readiness | Ethereum Foundation researchers | Ethlabs | Technical and monetary work moves into a treasury-backed R&D node. |

| Institutional sales and corporate adoption | EF go-to-market work | Ethereum Institutional | Corporate distribution moves into a dedicated nonprofit built for banks, asset managers and public companies. |

| Asset accumulation and public-market narrative | Crypto-native holders and ETF flows | ETH treasury firms such as Bitmine and Sharplink | The firms funding the new stack also benefit directly if ETH demand rises. |

Ethereum Institutional says its team already carries more than 500 institutional relationships across Tier-1 banks, asset managers, sovereign institutions, custodians, and market infrastructure providers.

Its Institutional Ethereum Forum drew more than 150 senior executives representing roughly $250 trillion in combined assets under management. That scale is the argument for building a standalone organization rather than running the work as a side project within the EF.

Handing corporate distribution and ETH advocacy to outside groups solves an execution disconnect, while it also means the firms with the largest ETH balance sheets finance the loudest voices selling Ethereum to Wall Street.

Convenience and independence pull in opposite directions, and Ethereum has chosen convenience.

Ethereum’s Wall Street machine is being rebuilt by the ETH treasuries that need it to work

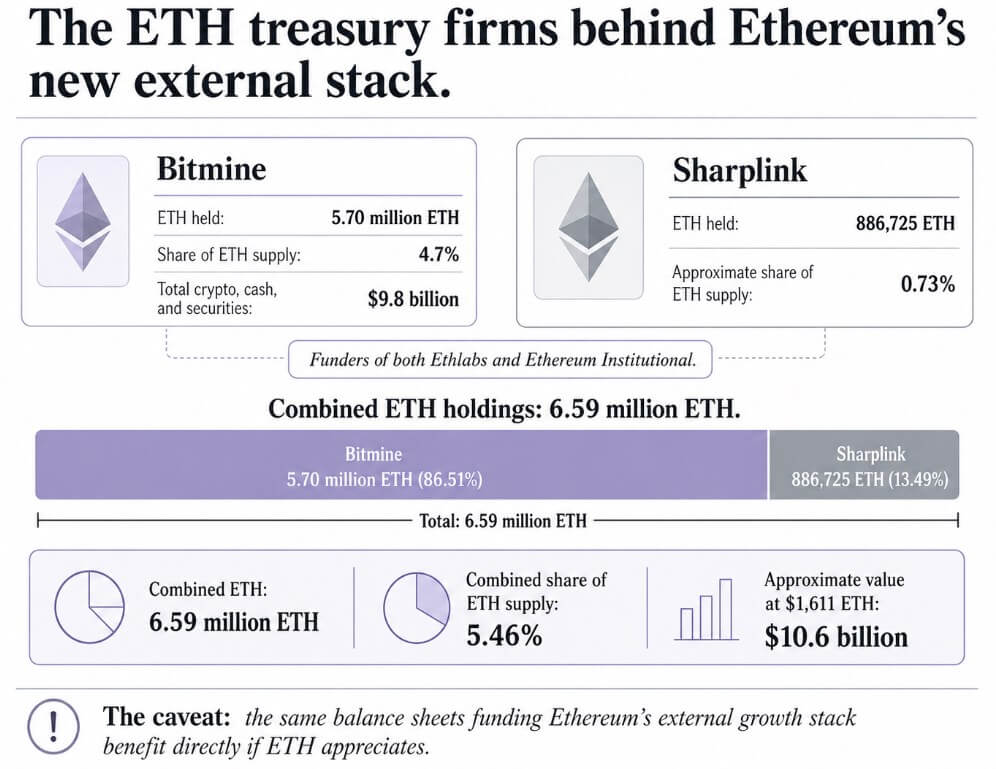

Bitmine currently holds 5.70 million ETH, 4.7% of the total supply, alongside cash and marketable securities, bringing its balance sheet to $9.8 billion. Sharplink holds 886,725 ETH, a position it added to on June 28 by purchasing 10,000 ETH at an average price of $1,611.

Combined, the two firms carry roughly 6.59 million ETH, about 5.46% of the 120.7 million ETH supply that Bitmine itself cites. At current prices, that stake is worth close to $10.6 billion, against Bitmine's market cap of $6.55 billion and Sharplink's market cap of over $1 billion.

Infographic detailing Bitmine and Sharplink's combined 6.59 million ETH holdings, worth about $10.6 billion, which fund Ethereum's new external growth organizations.

Infographic detailing Bitmine and Sharplink's combined 6.59 million ETH holdings, worth about $10.6 billion, which fund Ethereum's new external growth organizations.

Both firms benefit directly if the split works, since better infrastructure and cleaner institutional sales push ETH demand higher, and they hold enough ETH that a modest price move alters their balance sheets by hundreds of millions of dollars.

Joe Lubin, who backs both nonprofits and co-founded Ethereum itself, sits at the center of that alignment. The arrangement is a structure worth watching, since Bitmine and Sharplink have direct financial exposure to its success.

PeerDAS, already live, delivers roughly a tenfold increase in data availability capacity for layer-2 networks, while Glamsterdam, planned for the second half of 2026, targets base-layer scaling, parallel transaction processing, and larger block payloads.

A June 2026 academic paper measured the payoff so far, finding that transaction throughput on mainnet and layer-2s has doubled. Mainnet median fees fell from above $2 to below $0.02, and layer-2 median fees dropped more than 95% to roughly $0.0015.

Mainnet throughput stays below 100 transactions per second until 2034, and layer-2 networks overtake Solana's throughput only in March 2029, with lower median fees arriving by October 2026.

Ethereum's institutional case depends almost entirely on layer-2 execution and standards work, the kind of technical positioning Ethlabs exists to manage.

Two ways ETH's price rewrites this

The bull case rests on a scale that already exists, as Ethereum carries about $157 billion in stablecoin value on the network, over half of the global stablecoin supply, and roughly $37.2 billion in DeFi deposits, more than 62% of all blockchain-based DeFi value.

RWA.xyz ranks Ethereum at the top of tokenized real-world asset networks, with nearly $15.8 billion in distributed asset value, accounting for $31.52 billion across all tracked networks.

Citi projects the broader tokenization market will expand from about $17 billion today to $5.5 trillion by 2030, with a range of $2.7 trillion to $8.2 trillion. If Ethlabs keeps infrastructure in front of demand and Ethereum Institutional converts relationships into deployed capital, the treasury firms funding both start to resemble early stewards.

Ethereum becomes the default settlement venue for regulated digital assets, and its balance sheet benefits accordingly.

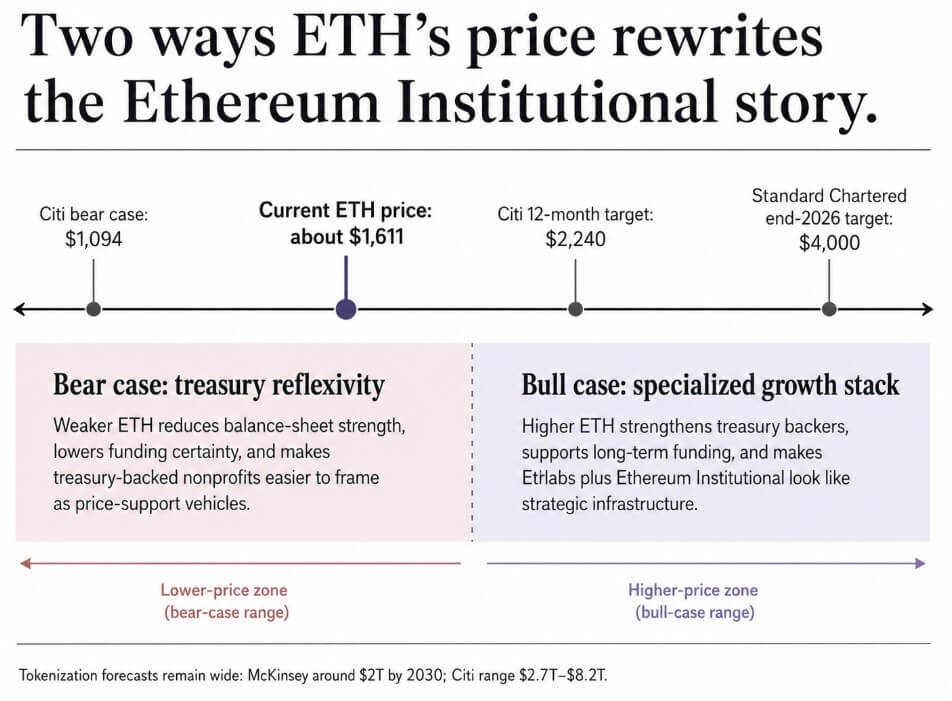

The bear case starts with price, since Citi cut its 12-month ETH target to $2,240 from $3,175, citing thin ETF appetite and negative flows, and set a bear scenario at $1,094 against ETH's current price near $1,611.

Standard Chartered disagrees sharply, holding to a $4,000 target by the end of 2026, but the disagreement itself shows how unsettled the near-term case is.

Infographic showing ETH price targets from $1,094 to $4,000, outlining bear and bull scenarios for Ethereum Institutional's treasury-backed funding model.

Infographic showing ETH price targets from $1,094 to $4,000, outlining bear and bull scenarios for Ethereum Institutional's treasury-backed funding model.

If ETH stays weak and treasury-firm equities trade at persistent discounts to their underlying holdings, Bitmine and Sharplink's ability to keep underwriting two nonprofits shrinks along with their balance sheets.

Ethlabs and Ethereum Institutional would probably keep operating. Funding certainty would drop, though, and both groups would have a harder time deflecting the argument that they exist to prop up ETH's price rather than build genuine institutional infrastructure.

Regulatory tailwinds help the bull case without guaranteeing it: the 2025 GENIUS Act provided US stablecoins with their first federal framework, and a consortium linked to Visa, Mastercard, and Coinbase launched a competing stablecoin, Open USD, once that framework existed.

That regulatory movement benefits every chain competing for institutional settlement volume.

McKinsey's more conservative tokenization forecast, around $2 trillion by 2030 against Citi's far larger range, is a reminder that even the bull case has real disagreement baked into it.

Ethereum solved its post-Foundation problem by building two new organizations. Both are funded by the companies with the most to gain from ETH going up, and both hold jobs a neutral steward could never do well.

That arrangement can produce exactly what it promises: better infrastructure, cleaner institutional access, and a chain that earns its position as the default settlement layer for tokenized finance.

It can also mean that Ethereum's expansion machine now runs on the same balance sheets it is supposed to expand.

Both are true at once, and where ETH's price sits a year from now decides which one dominates.

The post Ethereum is splitting into three power centers and ETH treasury firms are paying for two appeared first on CryptoSlate.

You May Also Like

Mizuho’s $130 Robinhood Price Target Says Crypto Is Underpriced

China Nabs Another Huione Group Core Member in Cambodia Extradition