South Africa’s taxman wants a cut of your crypto — Here’s what SARS’ new draft guide really says

The South African Revenue Service (SARS) has never doubted that it wants a share of crypto profits. What it has lacked, until now, is a coherent rulebook explaining exactly how that share gets calculated. On 1 July 2026, SARS released a draft guide to the taxation of crypto assets, an attempt to finally close the gap between an eight-year-old media statement and a market that has since exploded into staking, DeFi, arbitrage bots and NFT-adjacent tokens.

The guide isn’t law. It carries no binding force and creates no “practice generally prevailing”, as SARS states in its preface. But it is the clearest signal yet of how the taxman intends to interpret existing legislation, the Income Tax Act and the Eighth Schedule, when it looks at a crypto wallet. For African crypto investors and traders watching South Africa as a regional bellwether, that interpretive stance matters even beyond its borders.

At the heart of the guide sits a distinction South African tax law has wrestled with for a century: is a gain capital in nature, taxed at a friendlier effective rate of up to 36%, or revenue in nature, taxed at up to 45%? SARS confirms crypto assets get no special exemption from this fight. There’s no equivalent of the “three-year rule” that applies to shares under section 9C; buy and hold a coin for a decade, and you could still be assessed as a trader if your conduct says so.

What’s genuinely useful here is how far SARS goes in laying out the tells it will look for. Frequency of transactions, the absence of any yield beyond price appreciation, and the sheer volatility of the asset class are all treated as circumstantial evidence of trading intent. SARS draws a direct and slightly unflattering comparison between crypto and Krugerrands, walking through six historic gold-coin tax cases to argue that an asset offering “no return or low return” beyond its own appreciation is inherently more likely to attract a revenue finding. It’s an old analogy dressed up for a new asset class, but it’s coherent, and it gives taxpayers something concrete to test their own behaviour against.

Similarly, under the guideline, swapping one crypto asset for another, even without ever touching fiat currency, is a barter transaction and therefore a taxable event. Trade Bitcoin for Solana on Luno, and SARS treats that as if you sold the Bitcoin for its market value and immediately bought Solana with the proceeds.

This has real implications for anyone actively rebalancing a portfolio across trading pairs, assuming, as many still do, that tax only bites when crypto is converted back into rand.

SARS says mining, staking and getting paid in crypto attract tax

The guide also tackles income streams that African crypto users increasingly rely on. Mining rewards are treated as ordinary income at market value the moment they land in a wallet, full stop, regardless of whether the miner ever intended to trade them. Staking rewards follow the same logic under a “Proof-of-Stake” framework. Employers paying salaries partly in crypto must still withhold PAYE, and even a long-service bonus paid in Solana gets taxed as a fringe benefit, net of a modest R5 000 concession.

SARS cites Forbes data showing Bitcoin’s volatility running at roughly 4.8 times that of the S&P 500 and over five times that of gold, using the figure explicitly as evidence that crypto rarely fits a genuine long-term “capital preservation” story unless the taxpayer’s broader portfolio context supports it.

For all its detail, the draft is careful to say what it isn’t: not VAT guidance, not a binding ruling, and not a substitute for case-by-case analysis. Questions such as wallet-to-wallet transfers between a taxpayer’s own accounts are explicitly left open, dependent on the “specific facts of the transfer”. Given the pace of DeFi innovation, that caution is arguably realistic rather than evasive, but it also means taxpayers navigating genuinely novel structures will still need professional advice, not just this document.

Also read: A $2 trillion market cap loss made H1 2026 crypto’s worst half-year in four years

Although the guide hasn’t settled every argument crypto investors have with SARS, it removes a lot of the ambiguity that has allowed both taxpayers and advisors to interpret grey areas generously. Frequent traders, arbitrageurs and anyone earning crypto through mining or staking should treat this as confirmation that SARS is watching closely and has done its homework. For long-term holders, the message is equally clear: intention has to be demonstrable, not just declared, and the burden of proof sits with the taxpayer.

You May Also Like

Alleged Huione Money Laundering Boss Extradited to China

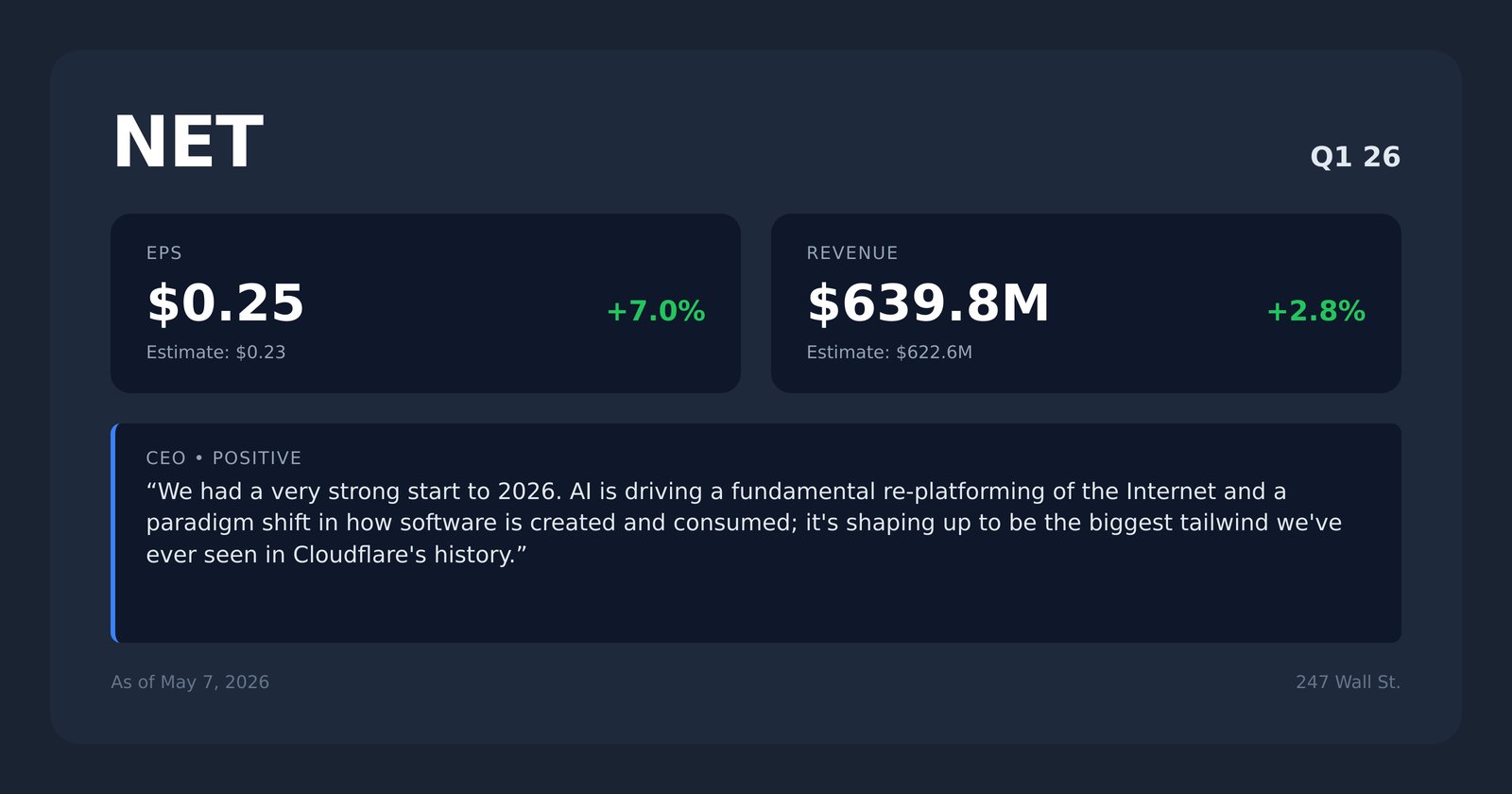

How Cloudflare Is Positioning for the AI Era