SoFi Price Prediction: The Stock Set for 13% Upside

The post SoFi Price Prediction: The Stock Set for 13% Upside appeared first on 24/7 Wall St..

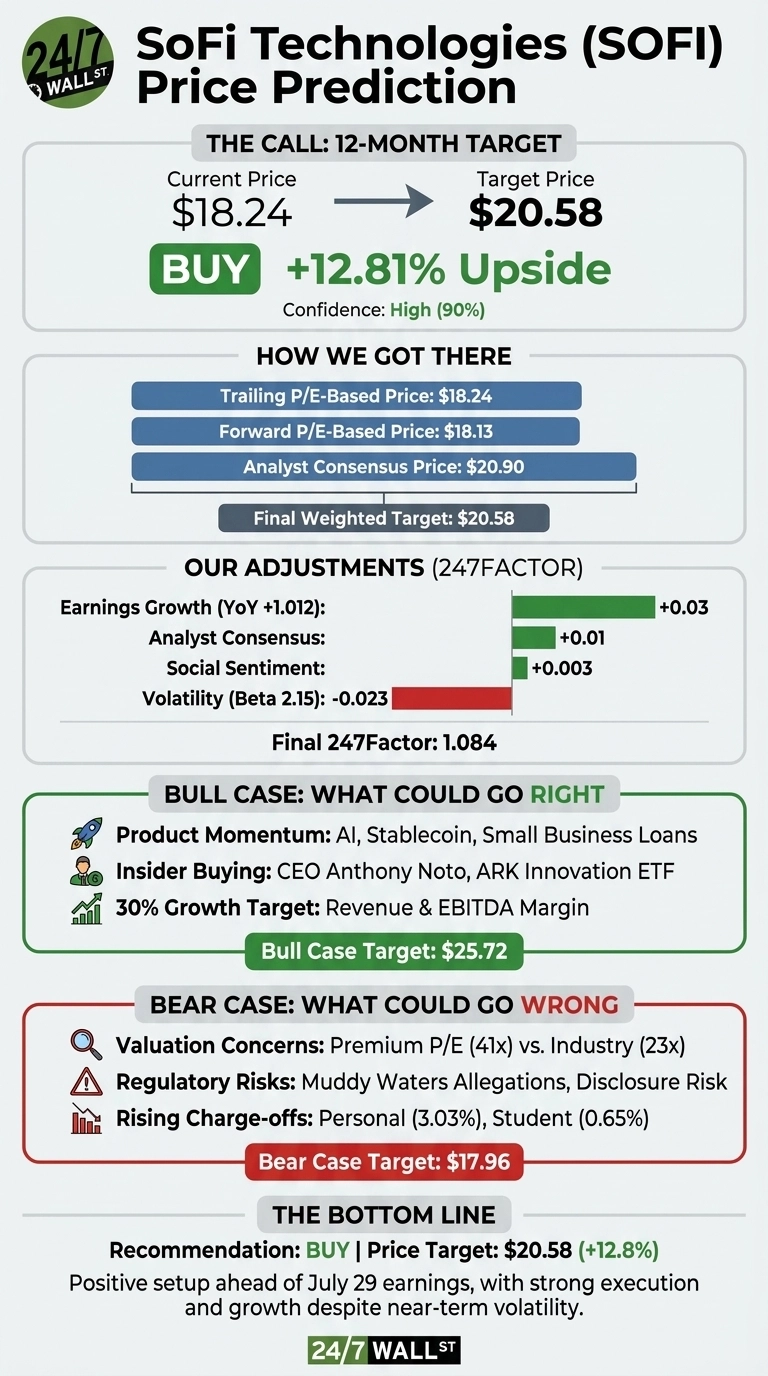

Our SoFi Technologies (NASDAQ:SOFI) price target sits above where the stock trades today, and I think the setup into the July 29 earnings report is more constructive than the recent selloff suggests.

SoFi has slid 30.33% year to date even as the underlying business posted its 18th consecutive quarter of the Rule of 40. That disconnect is where the opportunity lives.

The 24/7 Wall St. price target for SoFi is $20.58 over the next 12 months, implying 12.81% upside from the current $18.24 level. Our recommendation is buy, with a high (90%) confidence score.

24/7 Wall St.

24/7 Wall St.

| Metric | Value |

|---|---|

| Current Price | $18.24 |

| 24/7 Wall St. Price Target | $20.58 |

| Upside | 12.81% |

| Recommendation | BUY |

| Confidence Level | 90% |

From $28 to $15 and Back: The Setup Now

SoFi peaked near $28 in October 2025 before bottoming at $15.61 in May 2026. The stock has since clawed back 5.43% over the past week on the Composer AI acquisition and a new small business loans platform.

Q1 2026 delivered revenue of $1.10 billion, beating consensus by roughly $51.1M, with EPS of $0.12 and net income up 134.45% year over year. Loan originations hit a record $12.18 billion, up 68%, and members grew 35% to 14.7 million.

The Case for $25 and Higher

Bulls have real ammunition. Adjusted EBITDA was $340 million at a 31% margin, and 2026 guidance calls for adjusted revenue of $4.655 billion and adjusted EPS near $0.60. CEO Anthony Noto framed the trajectory bluntly: “Our strategy and execution continue to be unmatched by any company I can think of at our scale.”

Add the SoFiUSD stablecoin, the Mastercard settlement partnership, the Composer AI deal, and Big Business Banking, and the optionality is real. Our bull case scenario puts SoFi at $25.72 within a year.

What Could Go Wrong

The bear case starts with valuation. SoFi trades at a trailing P/E of 41 versus a credit services industry closer to 23. Personal loan charge-offs ticked up sequentially to 3.03% from 2.80%, student loan charge-offs rose to 0.65%, and net interest margin compressed 63 basis points.

The Muddy Waters report from March 2026 alleged accounting misstatements and undisclosed charge-off rates. Simply Wall St. pegs intrinsic value at $13.84. That said, the Technology Platform’s -27% segment revenue reflects one large client departure, and like-for-like growth was roughly 12% with 13 new partners signed in Q1. Our bear scenario lands at $17.96.

The Setup Favors Owners Here

The 24/7 Wall St. price target for SoFi is $20.58, our recommendation is buy, and confidence is high at 90%. The tipping factor is the mismatch between 30% guided growth and a stock trading closer to its 52-week low of $14.92 than its high of $32.73.

CEO Anthony Noto has been a consistent open-market buyer, and ARK just added 200,000+ shares. The bull thesis strengthens if the July 29 earnings report confirms roughly 30% revenue growth and stable credit. The thesis weakens if personal loan charge-offs cross 3.5% or the Muddy Waters allegations gain regulatory traction.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $20.58 |

| 2027 | $22.75 |

| 2028 | $24.90 |

| 2029 | $26.20 |

| 2030 | $27.53 |

These projections assume SoFi delivers on its 30% CAGR revenue path and continues to expand adjusted EBITDA margin. Significant upside could come from stablecoin adoption; downside risk lies with a credit cycle turn.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and SoFi Technologies didn’t make the cut. Grab the names FREE today.

The post SoFi Price Prediction: The Stock Set for 13% Upside appeared first on 24/7 Wall St..

You May Also Like

StakeStone (STO) Rockets 125%: What $981M Trading Volume Reveals

Marcoleta in Sandiganbayan custody over plunder case

M. Nasir celebrates 47 years in music with star-studded Bukit Jalil concert