CAVA Just Delivered 32% Revenue Growth While Most of Fast Casual Is Struggling

Key Stats for CAVA Group Stock

- 52-Week Range: $43.41 – $98.79

- Current Price: $90.99

- Street Mean Target: $92.00

- Street High Target: $110.00

- TIKR Annualized IRR (Mid): ~20% / year

Fast casual has had a rough stretch, as traffic across most major chains has been flat to negative, consumers have grown more selective, and a handful of well-known names have leaned on discounting just to hold their ground. CAVA Group walked into that environment in Q1 2026 and put up numbers that made the rest of the category look sideways.

Revenue grew 32.2% year over year to $438.3 million, same-restaurant sales climbed 9.7%, and guest traffic was up 6.8%. That last number is the one that matters most right now. In a sector where traffic growth has become scarce, CAVA (CAVA) is consistently producing it at scale. Analysts at UBS, Baird, Stifel, and Argus all raised their price targets in the days that followed.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

The Q1 Numbers That Turned Heads

The traffic story is worth unpacking because same-restaurant sales growth can come from two places: more customers walking through the door, or higher prices. CAVA’s 9.7% comp was driven primarily by the former, with traffic accounting for 6.8 percentage points of that gain.

CEO Brett Schulman noted on the Q1 call that CAVA has taken lower prices than peers since 2019, with cumulative increases running below inflation. The brand is pulling customers in on the strength of the product, not by squeezing the check.

Adjusted EBITDA rose 37.6% to $61.7 million, beating the Street by nearly 8%. The company opened 20 net new restaurants in the quarter, bringing the total to 459 locations, with new units averaging $3 million in volume at 100% productivity or better almost immediately.

CAVA Group Total Revenues, EBITDA. (TIKR)

CAVA Group Total Revenues, EBITDA. (TIKR)

The revenue and EBITDA trajectory in that chart captures the operating leverage story in a single frame. Revenue has compounded from $500 million in 2021 to $1.18 billion in 2025, while EBITDA climbed from near breakeven to $134 million over the same period. The model is working.

See historical and forward estimates for CAVA stock (It’s free!) >>>

Expansion Is the Engine, but Margins Are the Debate

At 459 locations against a target of 1,000 by 2032, there is still a long runway ahead. Management raised full-year 2026 guidance to 75-77 net new restaurant openings, and the company announced plans to hire more than 2,500 employees this year to support that pace.

Restaurant-level profit margins held at 25.1% in Q1, flat year over year as efficiency gains were offset by higher delivery costs, wage investments, and the rollout of the Assistant General Manager role now in place at more than half of CAVA’s locations.

Full-year margin guidance of 23.7% to 24.3% reflects a roughly 100 basis point headwind from the new pomegranate glazed salmon offering and an additional 20 to 40 basis point drag from energy costs. These are deliberate investments in menu innovation and infrastructure, not signs of a business losing control of its cost structure.

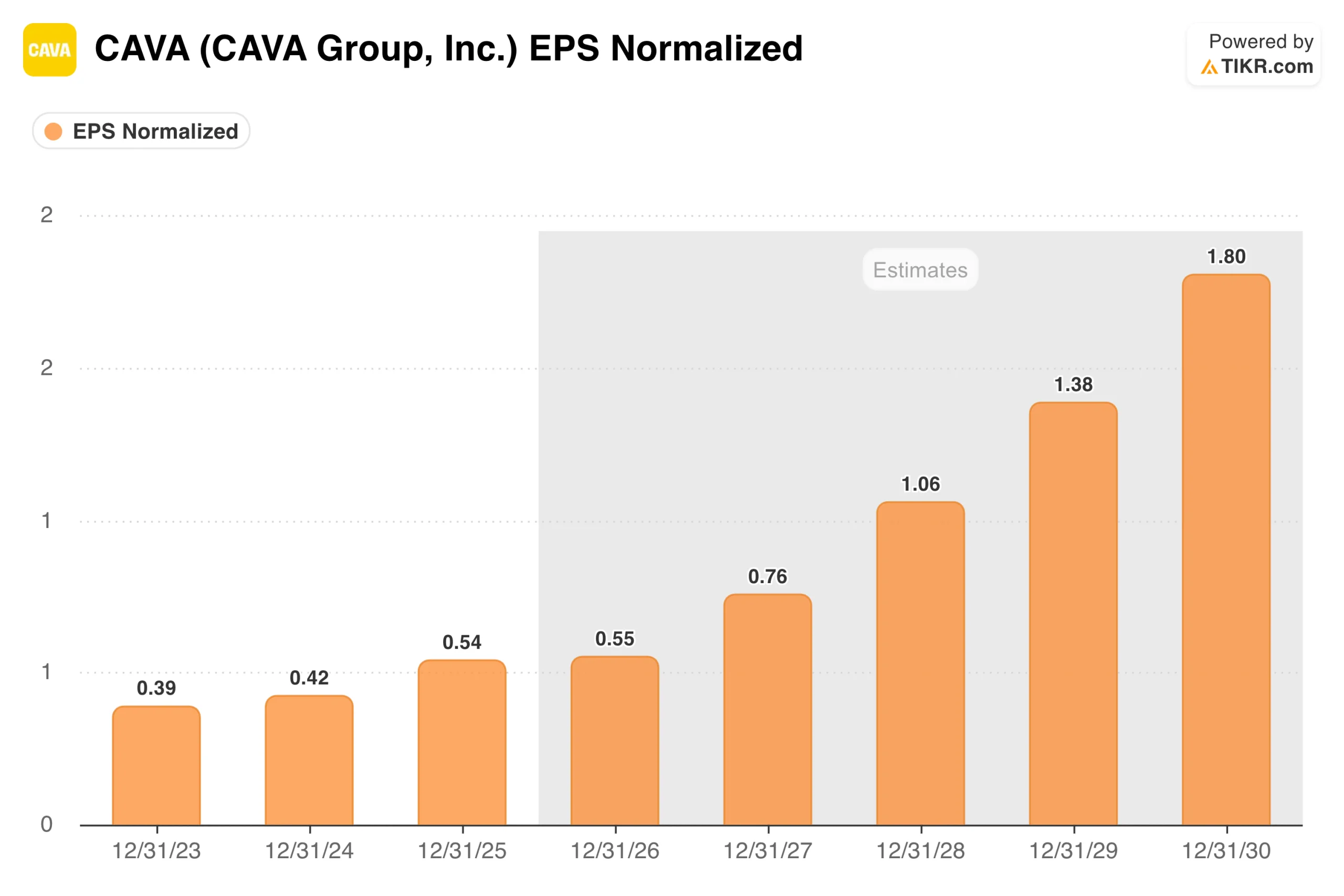

CAVA EPS Normalized. (TIKR)

CAVA EPS Normalized. (TIKR)

Consensus has EPS growing from $0.54 in 2025 to around $0.55 in 2026, then accelerating toward $1.80 by 2030 as the unit count scales and operating leverage builds. The near-term flatness reflects those margin investments, management is accepting some short-term pressure on profitability in exchange for a larger, better-staffed restaurant base.

See how CAVA performs against its peers in TIKR (It’s free!) >>>

Priced for Perfection or Priced for What’s Coming

At around $91, CAVA trades at roughly 149 times forward earnings and about 52 times forward EBITDA, well above Chipotle and every other name in the fast-casual peer group. That premium is either the most important thing about the stock or a distraction from what the business is actually building, depending on your time horizon.

CAVA Valuation Model. (TIKR)

CAVA Valuation Model. (TIKR)

TIKR’s valuation model targets around $213 per share in the mid case, representing a potential total return of around 134% over the next 4.5 years at roughly 20% annualized.

The low case arrives near $290 at about a 14% IRR, the high case projects toward $560 at close to 24% annually. Across all three scenarios, returns are driven by earnings growth rather than multiple expansion. The model assumes modest P/E compression in the base case, meaning consistent execution is the price of admission, not a rerating.

The scenario range skews to the upside if same-store sales hold and new-unit productivity continues to outperform. Revenue growth of around 19% annually through 2035 is the key assumption, with net income margins expanding from around 5% today toward 7% as fixed costs get absorbed across a larger restaurant base.

What the Bulls Are Betting On

- Traffic growth is durable. CAVA has produced positive traffic comps where most peers have not, and its below-inflation pricing strategy leaves room to take more price without pushing customers away.

- Unit economics hold at scale. New stores are hitting $3 million AUV at full productivity from day one, suggesting the brand translates cleanly across new geographies.

- The Chipotle comparison still has legs. Chipotle had roughly 500 locations when it went public and now operates more than 3,700. CAVA is earlier in that journey with a category tailwind that is arguably stronger today.

- Technology is building a moat. The rollout of CAVA Core and CAVA Current is designed to drive personalization and repeat visits in ways legacy restaurant operators have not prioritized.

What the Bears Are Watching

- The valuation leaves no margin for error. At roughly 149 times forward earnings, any stumble in same-store sales, margins, or new unit productivity will be punished quickly.

- Near-term earnings growth is essentially flat. The EPS chart shows 2026 estimates barely above 2025 actuals, which is a hard pill to swallow at this multiple.

- Margin investments are real costs. Salmon, AGM rollout, wage increases, and energy headwinds are all hitting simultaneously, and the full-year margin guide sits below last year’s restaurant-level result.

- The Street is already skeptical. With the stock at $91 and the mean analyst target at $92, the market has essentially caught up to where most models land.

Review analysts’ growth forecasts and price targets for CAVA stock (It’s free!) >>>

Should You Invest in CAVA Group?

CAVA is one of the clearest growth stories in the restaurant sector, and Q1 showed the business is still executing.

Traffic is growing, new stores are productive, and the path to 1,000 locations is intact. The harder question is whether any of that is a surprise at this valuation, with the stock already up more than 100% off its lows and the mean analyst target sitting right at the current price.

For investors with a long time horizon and conviction in the category, CAVA remains one of the more compelling growth vehicles available. For those focused on near-term value, the entry point is a genuine challenge.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

Ayrıca Şunları da Beğenebilirsiniz

Crypto Hack: Drift Protocol Drained Over $200M in Private Key Breach

XRP Ledger Upgrade Progress Puts $3.06 Resistance in Focus

Ripple News: Flutterwave Stake Opens RLUSD and XRP Ledger Push in Africa

Popüler Haberler

Daha fazla